Common Stock and Accounting For Stockholders' Equity

Common Stock

If a corporation has issued only one type, or class, of stock it will be common stock. ("Preferred stock" is discussed later.) While "common" sounds rather ordinary, it is the common stockholders who elect the board of directors, vote on whether to have a merger with another company, and get huge returns on their investment if the corporation becomes successful.

When an investor gives a corporation money in return for part ownership, the corporation issues a certificate of ownership interest to the stockholder. This certificate is known as a stock certificate, capital stock, or stock. (Today the larger corporations will handle the shares or stock electronically.)

Stock is the evidence of an ownership interest, it is not a loan to the corporation; stock does not come due ormature. A stockholder owns the stock until he/she decides to sell it. If stockholders want to sell their stock, they must find a buyer usually through the services of a stockbroker. Nowhere on the stock certificate is it indicated what the stock is worth (or what price was paid to acquire it). In a market of buyers and sellers, the current value of any stock fluctuates moment-by-moment.

A corporation's accounting records are involved in stock transactions only when the corporation is the issuer, seller, or buyer of its own stock. For example, if 500,000 shares of Apple Computer stock are traded on the stock exchange today, and if none of those shares is issued, sold, or repurchased by Apple Computer, then Apple Computer's accounting records are not affected. The corporation will go about its routine business operations without even noticing that there were some changes in its ownership.

Shares

Some investors may have large ownership interests in a given corporation, while other investors own a very small part. To keep track of each investor's ownership interest, corporations use a unit of measurement referred to as a "share" (or "share of stock"). The number of shares that an investor owns is printed on the investor's stock certificate. This information is also noted in the corporate secretary's record, a record which is not connected to the corporation's accounting records.

The ratio of investors to stock owned is different for every corporation and it may change many times per day depending on who is selling or buying stock. If an investor owns 1,000 shares and the corporation has issued and has outstanding a total of 100,000 shares, the investor is said to have a 1% ownership interest in the corporation. The other owners have the combined remaining 99% ownership interest.

Authorized shares

When a business applies for incorporation to a secretary of state, its approved application will specify the classes (or types) of stock, the par value of the stock, and the number of shares it is authorized to issue. (Shares are often issued in exchange for cash. However, shares of stock can be issued in exchange for services or plant assets.) When its articles of incorporation are prepared, a business will often request authorization to issue a larger number of shares than what is immediately needed. By planning ahead this way, the business avoids the inconvenience of having to go back to the state if and when more shares are needed to raise more capital.

To illustrate, assume that the organizers of a new corporation need to issue 1,000 shares of common stock to get their corporation up and running. They keep in mind, however, that in one year they will need to issue additional shares to fund a planned factory expansion. Five years from now they foresee buying out another company and realize they will need to issue more shares at that time for the acquisition. As a result, they decide that their articles of incorporation should authorize 100,000 shares of common stock, even though only 1,000 shares will be issued at the time that the corporation is formed.

Issued shares

When a corporation sells some of its authorized shares, the shares are described as "issued." The number of issued shares is often considerably less than the number of authorized shares.

Corporations issue (or sell) shares of stock to obtain cash from investors, to acquire another company (the new shares are given to the owners of the other company in exchange for their ownership interest), to acquire certain assets or services, and as an incentive/reward for key officers of the corporation.

The "par value" of a share of stock is sometimes defined as the legal capital of a corporation. The par value of common stock is usually a very small insignificant amount that was required by state laws many years ago. Because of those existing laws whenever a share of stock is issued, the par value is recorded in a separate stockholders' equity account in the general ledger. Any proceeds that exceed the par value are credited to another stockholders' equity account. This required accounting (discussed later) means that you can determine the number of issued shares by dividing the balance in the par value account by the par value per share.

Outstanding shares

If a share of stock has been issued and has not been reacquired by the corporation, it is said to be "outstanding." For example, if a corporation initially sells 2,000 shares of its stock to investors, and if the corporation did notreacquire any of this stock, this corporation is said to have 2,000 shares of stock outstanding. The number of outstanding shares is always less than or equal to the number of issued shares. The number of issued shares is always less than (or equal to) the authorized number of shares.

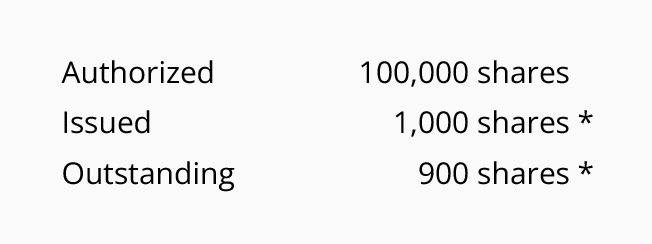

Here is a mathematical presentation:

When a corporation reacquires shares of its own stock and does not retire them, the corporation is said to have "treasury stock." (Treasury stock will be discussed later.) The number of outstanding shares is equal to the number of issued shares minus the number of treasury shares.

Here are the terms in descending order (largest to smallest) based on hypothetical amounts:

* The difference between the ISSUED shares and the OUTSTANDING shares is the number of shares of TREASURY STOCK (100 shares in this example).

Accounting For Stockholders' Equity

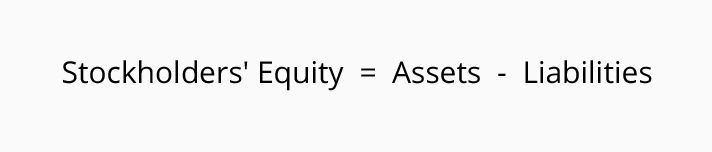

A corporation's balance sheet reports its assets, liabilities, and stockholders' equity. Stockholders' equity is the difference (or residual) of assets minus liabilities.

Because of the cost principle (and other accounting principles), assets are generally reported on the balance sheet at cost (or lower) amounts. As a result, it would be incorrect to assume that the total amount of stockholders' equity is equal to the current value, or worth, of the corporation. (For a more thorough discussion of the balance sheet, see Explanation of Balance Sheet.)

Because of legal requirements, the stockholders' equity section of a corporation's balance sheet is more expansive than the owner's equity section of a sole proprietorship's balance sheet. (For example, state laws require that corporations keep separate in their records the amounts received through investors from the amounts earned through business activity.) State laws may also require that the par value be reported in a separate account.

Below are the items that a corporation is required to report on its balance sheet in the stockholder's equity section. We will discuss them in the order they would appear on a balance sheet:

- Paid-in Capital (also referred to as Contributed Capital)

- Retained Earnings

- Treasury Stock

- Accumulated Other Comprehensive Income

Vo Thi Thuy Linh

Source: accountingcoach.com

» Tin mới nhất:

- Nhận biết "Điểm mù" trong đầu tư chứng khoán (24/04/2024)

- Kho vũ khí tuyệt vời để xây dựng kỹ năng viết tiếng Anh cho sinh viên (18/04/2024)

- CÁC YẾU TỐ BỊ LOẠI TRỪ KHI TÍNH GDP (18/04/2024)

- Chiến lược tăng trưởng quốc tế của Tesco (18/04/2024)

- Barra tại GM đối mặt với những thách thức (18/04/2024)

» Các tin khác:

- NHƯỢNG QUYỀN THƯƠNG HIỆU (18/12/2014)

- Các nhân tố ảnh hưởng đến nghiệp vụ Bao thanh toán (tiếp theo) (18/12/2014)

- Các nhân tố ảnh hưởng đến nghiệp vụ Bao thanh toán (18/12/2014)

- Accrued Interest (18/12/2014)

- Introduction to Bonds Payable (18/12/2014)

- Các bước trưởng thành của Nhà đầu tư_Giai đoạn 3-WHY (tt) (18/12/2014)

- Các bước trưởng thành của Nhà đầu tư_Giai đoạn 3-WHY (18/12/2014)

- Bảng tính nháp (worksheet) - cơ sở để lập báo cáo tài chính (phần 2) (18/12/2014)

- Bảng tính nháp (worksheet) - cơ sở để lập báo cáo tài chính (Phần 1) (18/12/2014)

- Xác định sức mạnh cạnh tranh của các nguồn lực và năng lực của công ty (17/12/2014)