Reporting Unusual Items

Income statements (whether single-step or multiple-step) report nearly all revenues, expenses, gains, and losses.

Sometimes rare or extraordinary events will occur during the income statement's time interval along with the normally recurring events. It's helpful to the reader of the statement if these unique items are segregated into a special section near the bottom of either the single-step or multiple-step income statement. These unique or rare items are:

1. Discontinued Operations

2. Extraordinary Items

When recording these items near the bottom of an income statement, it's required that you present them in the same order as they appear above. However, it is rare for a company to have either one of these items, and it is highly unlikely that a company will have both.

1. Discontinued operations pertains to the elimination of a significant part of a company's business, such as the sale of an entire division of the company. (Eliminating a small portion of product line does not qualify as a discontinued operation.)

2. Extraordinary items includes things that are unusual in nature and infrequent in occurrence. A loss due to an earthquake in Wisconsin would certainly be extraordinary. A loss due to a foreign country taking over a U.S. oil refinery in that country would be an extraordinary item.

If an item is unique and significant but it does not meet the criteria for being both "unusual and infrequent," the item must remain in the main section of the income statement; it can however be shown as a separate line item. For example, if a company suffers a $40,000 loss due to a strike by its workers, the $40,000 cannot be shown as an extraordinary item since it is not unusual in nature for a strike to occur. The $40,000 may be shown as a separate line item, but it must be positioned in the main portion of the income statement.

Two additional examples of situations that do not qualify as extraordinary items are (1) the loss from frost damage to a Florida citrus crop and (2) the write-down of inventory from cost to a lower amount. Apparently the frost in Florida is not unusual in nature and not infrequent. Similarly, it's not unusual for items in inventory to have a current value lower than its cost. Although these things maybe significant, unusual, and important, they do not belong in the section containing extraordinary items.

Below is an example of a single-step income statement containing an extraordinary item. (If this were a corporation, income tax expenses would be part of the income statement and an extraordinary gain would be reduced by the income tax expense associated with the gain; an extraordinary loss would be reduced by the income tax savings associated with the loss.) See net of tax.

Note that even in a single-step format shown above, the extraordinary item is separated out and added to the end of the income statement. The same would be true for discontinued operations.

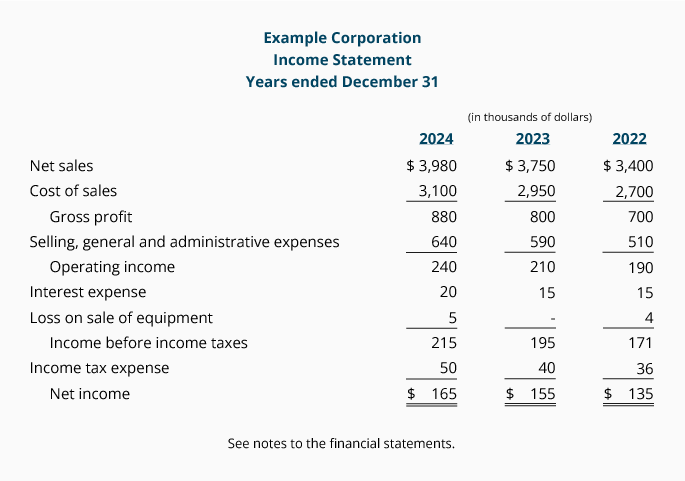

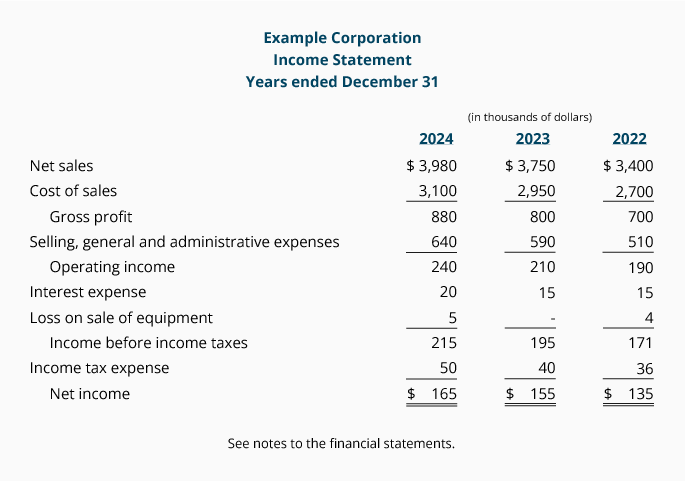

Below is a multiple-step income statement containing discontinued operations and an extraordinary item. (If this were a corporation, income tax expenses would be part of the income statement; the two unique items would be reduced by the income tax effect associated with each item.)

Note that the two unique items are shown near the bottom of the income statement. This is where the items should appear on both single-step and multiple-step statements.

» Tin mới nhất:

- Những Website Check Lỗi Ngữ Pháp Tiếng Anh Chất Lượng (18/05/2024)

- The writing process and assessment (18/05/2024)

- Những kinh nghiệm làm đồ án dành cho sinh viên kiến trúc (18/05/2024)

- Vai trò của các công cụ khuyến mãi đối với hành vi tiêu dùng (18/05/2024)

- Quyết định đầu tư chứng khoán và các mô hình nghiên cứu (18/05/2024)

» Các tin khác:

- Pressure for change originates in the environment (18/06/2015)

- Management of radical change likely to differ from the management of incremental change (18/06/2015)

- Tìm hiểu về chứng khoán phái sinh (17/06/2015)

- Quản trị doanh nghiệp cần nổ lực theo thông lệ quốc tế (17/06/2015)

- PBL Implementation of Computer Simulation in the Teaching of Strategic Management at Duy Tan University (P.2) (17/06/2015)

- PBL Implementation of Computer Simulation in the Teaching of Strategic Management at Duy Tan University (P.1) (17/06/2015)

- Sự mẫu thuẩn trong chế độ kế toán Việt Nam hiện hành giữa thông tư số 200/2014/TT-BTC và quyết định số 48/2006-QĐ-BTC (17/06/2015)

- Đối tượng hạch toán kế toán và những bất cập trong mã hóa tài khoản trong hệ thống tài khoản kế toán Việt Nam (17/06/2015)

- How to Get an Accounting Job With No Experience (17/06/2015)

- How to Learn Accounting Software (17/06/2015)