Disposal of Assets

If a company disposes of (sells) a long-term asset for an amount different from its recorded amount in the company's accounting records (its book value), an adjustment must be made to net income on the cash flow statement.

For example, let's say a company sells one of its delivery trucks for $3,000. That truck is shown on the company records at its original cost of $20,000 less accumulated depreciation of $18,000. When these two amounts are combined ("netted together") the net amount is known as the book value (or the carrying value) of the asset. In the example, the book value of the truck is $2,000 ($20,000 - $18,000).

Because the proceeds from the sale of the truck are $3,000 and the book value is $2,000 the difference of $1,000 is recorded in the account Gain on Sale of Truck—an income statement account. The transaction has the effect of increasing the company's net income. If the truck had sold for $1,500 ($500 less than its $2,000 book value), the difference of $500 would be reported in the account Loss on Sale of Truck and would reduce the company's net income.

One of the rules in preparing a statement of cash flows is that the entire proceeds received from the sale of a long-term asset must be reported in the second section of the statement, the investing activities section. This presents a problem because any gain or loss on the sale of an asset is also included in the company's net income which is reported in the first section—operating activities. To avoid double counting, each gain isdeducted from net income and each loss is added to net income in the operating activities section of the cash flow statement.

Let's illustrate this by returning to Good Deal Co.'s activities.

July Transactions and Financial Statements

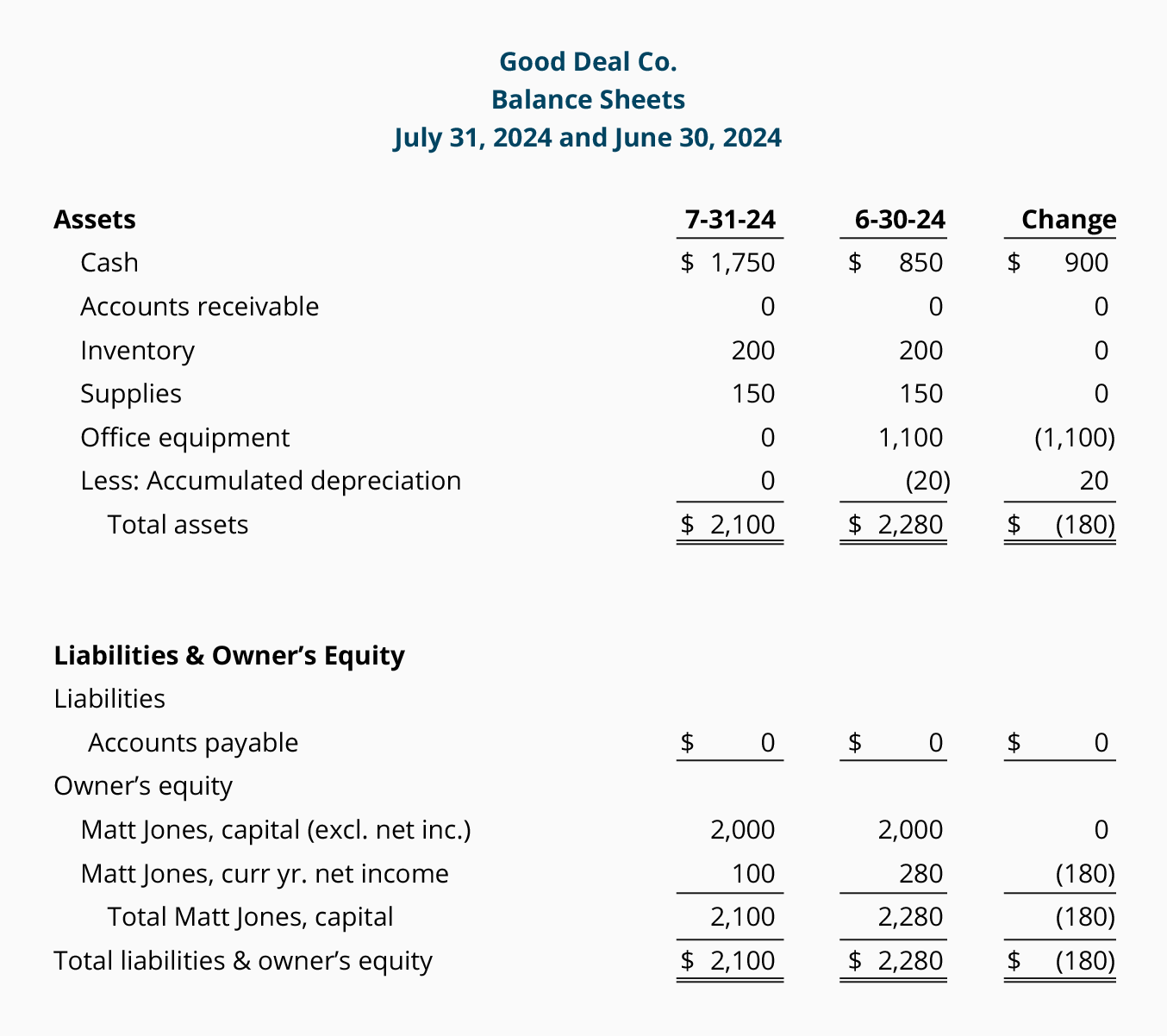

On July 1 Matt decides that his company no longer needs its office equipment. Good Deal used the equipment for one month (May 31 through June 30) and had recorded one month's depreciation of $20. This means the book value of the equipment is $1,080 (the original cost of $1,100 less the $20 of accumulated depreciation). On July 1 Good Deal sells the equipment for $900 in cash and records a loss of $180 in the accountLoss on Sale of Equipment on its income statement. There were no other transactions in July.

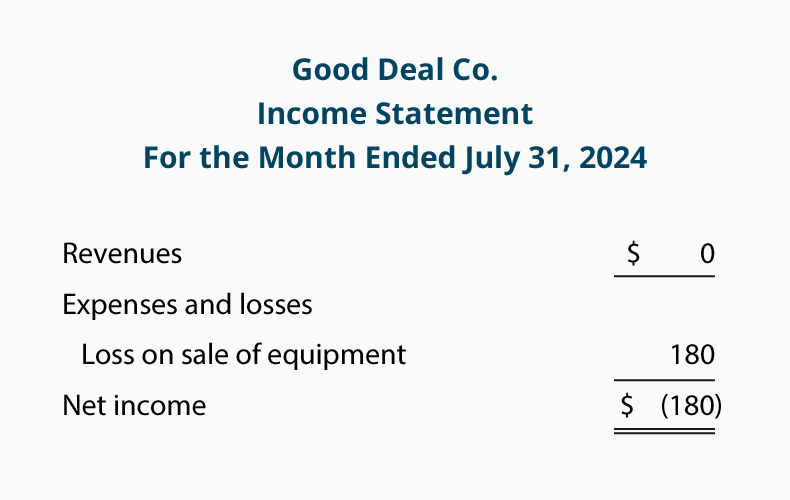

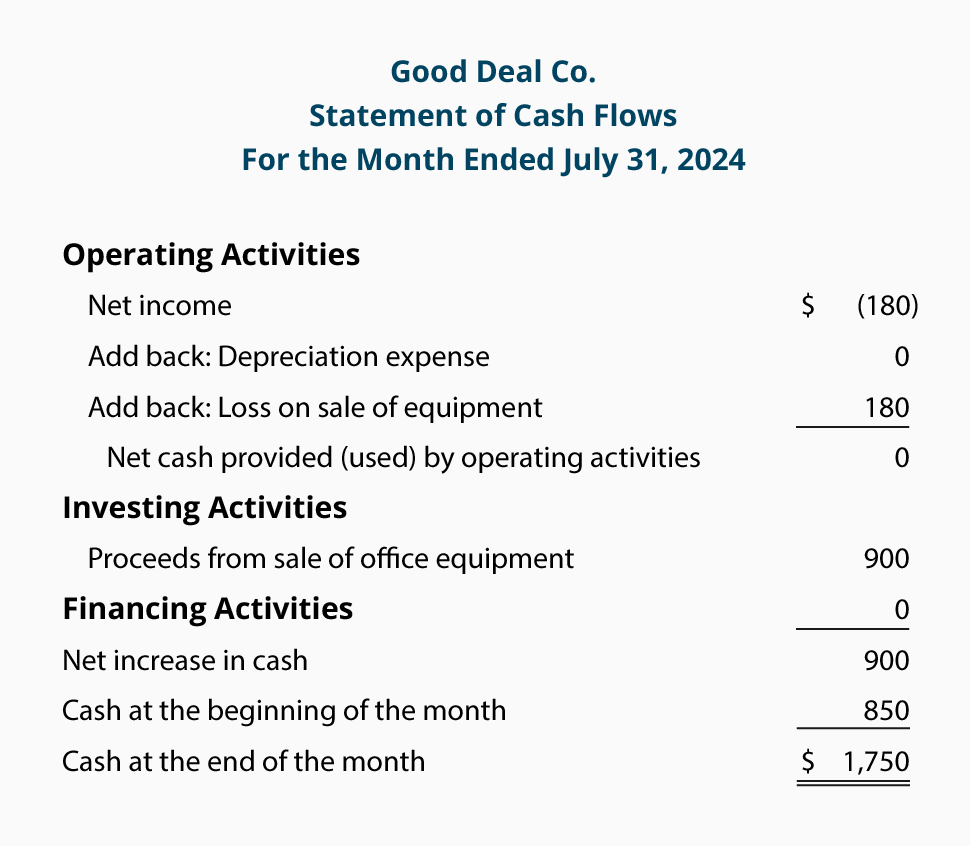

The income statement and the statement of cash flows for the month of July illustrate how the disposal of the equipment is reported:

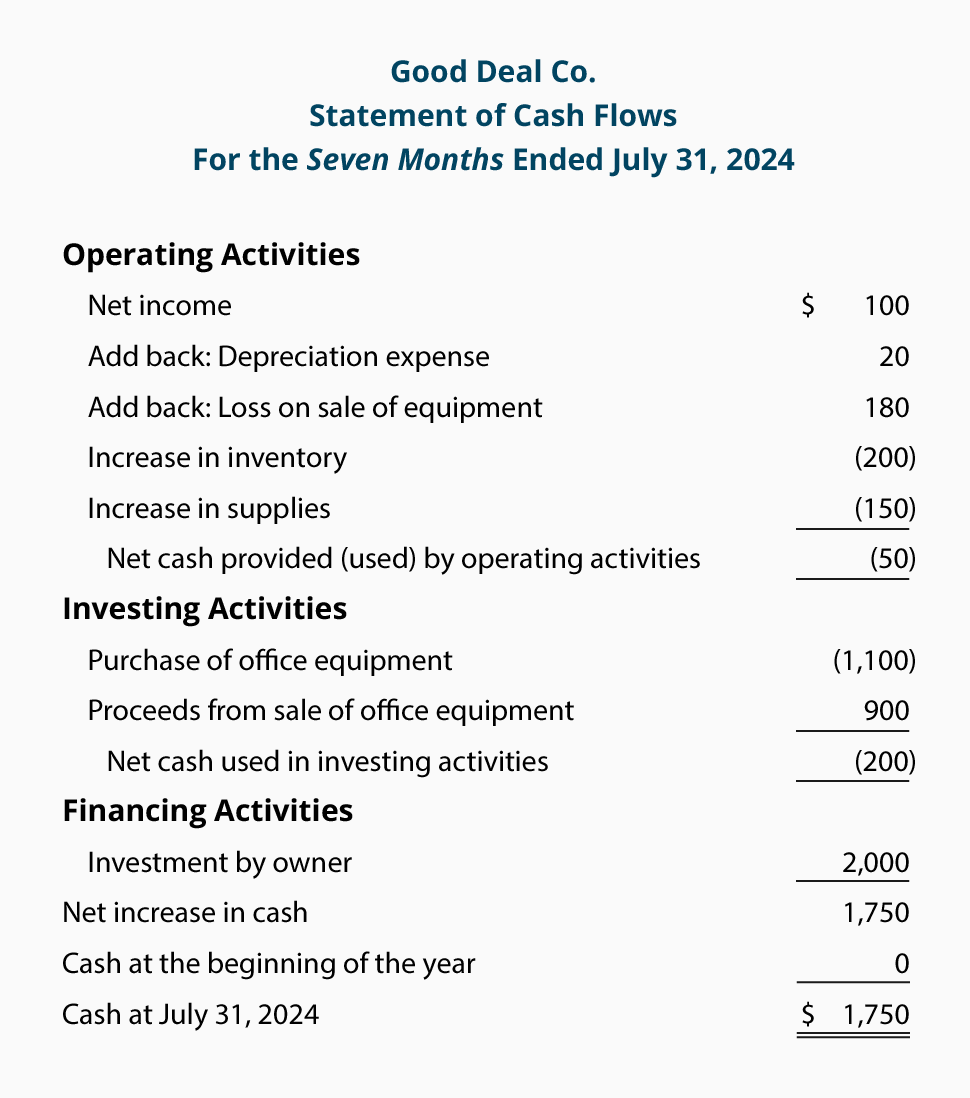

Let's review the cash flow statement for the month of July 2014:

- Net income for July was a net loss of $180. There were no revenues, expenses, or gains, but there was an entry of $180 in the account Loss on Sale of Equipment.

- There was no depreciation expense in July, and current assets and current liabilities did not change in July, so cash was not affected. (We could have omitted the line "Depreciation Expense".)

- There was no cash provided or used by operating activities.

- Good Deal received $900 from the sale of its office equipment.

- There was no change in long-term liabilities or owner's equity during July (other than the $180 loss on sale of equipment).

The summation of the amounts on the cash flow statement is a positive cash inflow of $900. This amount agrees to our check figure—the increase in the Cash account balance from June 30 to July 31.

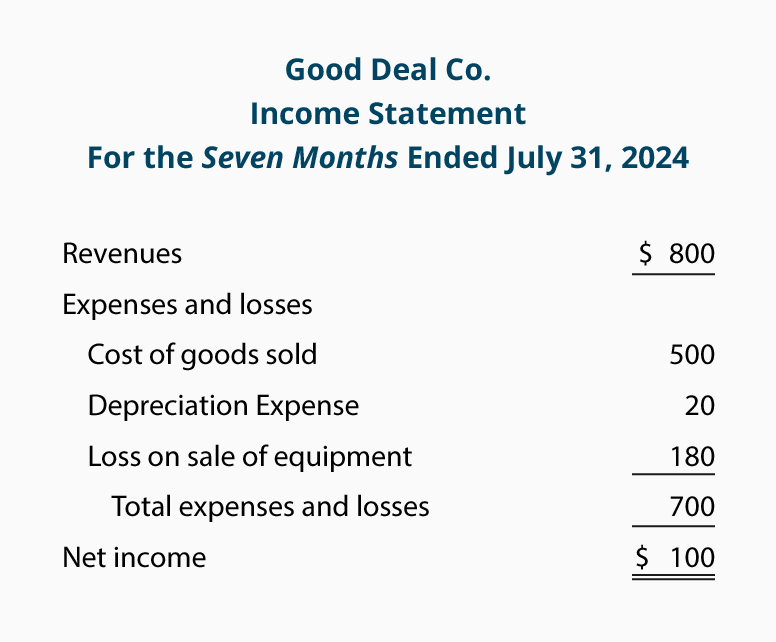

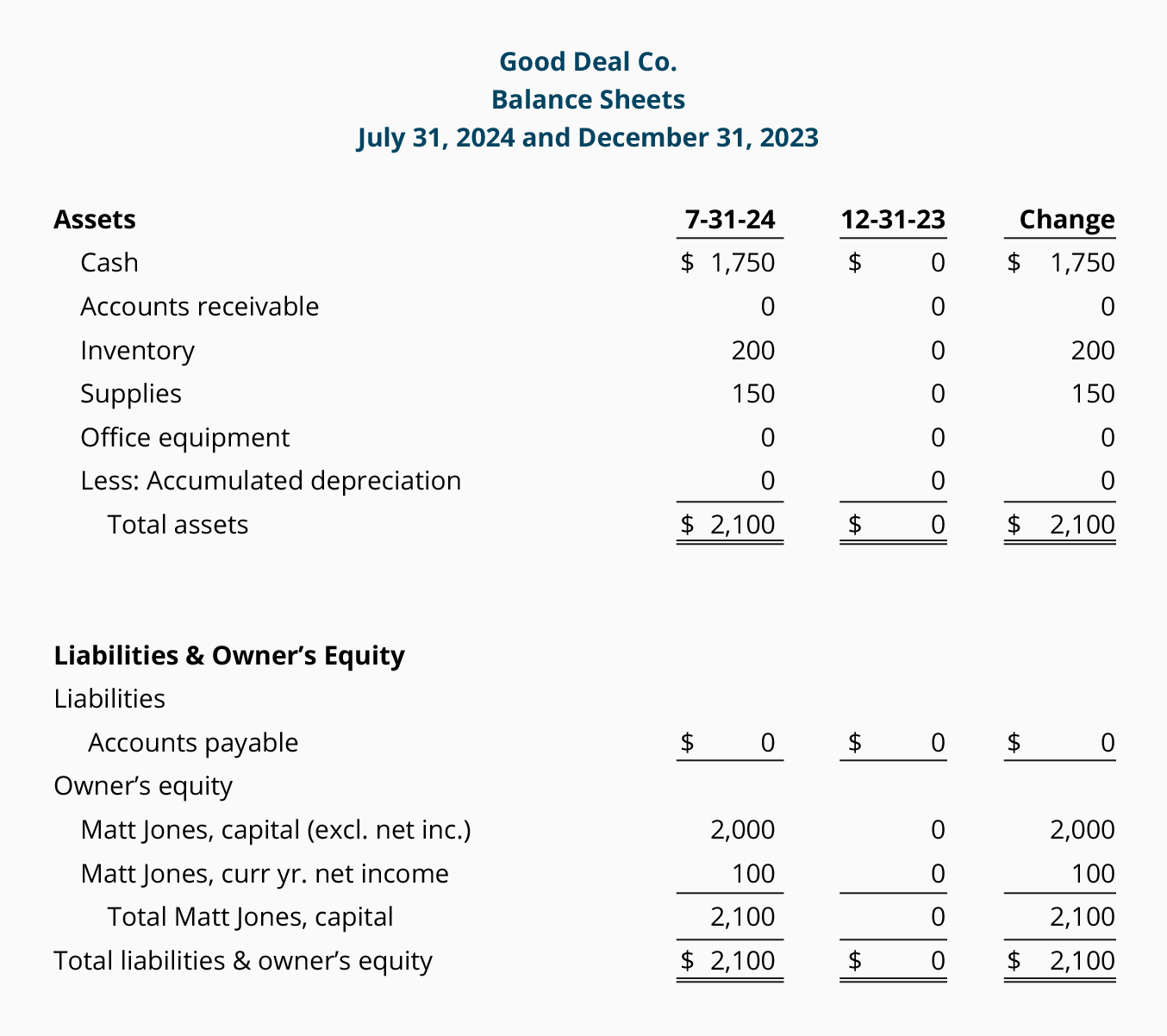

Let's review the cash flow statement for the seven months of January through July 2014:

- Net income for the seven months is $100. This includes revenues, gains, expenses, and losses.

- Included in the net income for the seven months is $20 of depreciation expense. This expense reduced net income but did not reduce the Cash account; therefore we add the $20 depreciation expense to the net income.

- Also included in net income is the $180 entry into the Loss on Sale of Equipment account. This loss was reported on the income statement thereby reducing net income but not reducing cash. (The cash received from the sale of the equipment appears in its entirety under the investing activities section of the cash flow statement.)

- Inventory on July 31 is $200 (4 calculators at a cost of $50 each). Since the company began with no inventory, this increase in the Inventory account means that $200 of cash was used to increase inventory.

- Supplies increased from none to $150. The increase in the Supplies account is assumed to have had a negative effect of $150 on the Cash account.

- Combining the amounts so far, we see that the cash from operating activities is a negative $50. In other words, rather than providing cash, the operating activities used $50 of cash.

- There is cash outflow (or payment) of $1,100 to purchase the office equipment on May 31 and the $900 of cash inflow (or receipt) from the sale of the office equipment on July 1. Combining these two amounts results in the net outflow ("cash used in investing activities") of $200.

- There was an owner's investment of $2,000 made on January 2.

The statement of cash flow's bottom line amount of $1,750 results from combining the amount totals of the previous three sections—operating, investing, and financing activities. This $1,750 agrees to the check figure—the difference in the Cash account balance from the beginning of January to July 31.

» Tin mới nhất:

- Cách GHI – ĐỌC dữ liệu từ tệp tin trong ngôn ngữ Java (18/12/2024)

- Những Website Check Lỗi Ngữ Pháp Tiếng Anh Chất Lượng (18/05/2024)

- The writing process and assessment (18/05/2024)

- Những kinh nghiệm làm đồ án dành cho sinh viên kiến trúc (18/05/2024)

- Vai trò của các công cụ khuyến mãi đối với hành vi tiêu dùng (18/05/2024)

» Các tin khác:

- Evaluating Business Investments (14/01/2016)

- Các font chữ nên và không nên dùng khi viết CV (13/01/2016)

- “Lý thuyết Nhân tài 3C” (3C Talent Formula) (13/01/2016)

- People CMM – mô hình trưởng thành về năng lực (P2) (13/01/2016)

- People CMM – mô hình trưởng thành về năng lực (P1) (13/01/2016)

- 7 XU HƯỚNG MARKETING ONLINE CHIẾM ƯU THẾ TRONG NĂM 2016. (30/12/2015)

- Chức năng của tiền tệ (18/12/2015)

- Lịch sử phát triển của tiền tệ (18/12/2015)

- Các chiều hướng văn hóa khác biệt giữa các quốc gia (18/12/2015)

- Các dạng phong cách lãnh đạo cơ bản (18/12/2015)