Related Expense or Asset

The vendor invoices received by a company could involve the following:

- A vendor invoice may be a bill for a repair or maintenance service. The vendor's credit terms allow the company to pay 30 days after the date of the service. Since repairs and maintenance do not create more assets, the cost of the service should be reported on the income statement as an expense. Under the accrual method of accounting the expense is reported in the accounting period in which the service occurred (not the period in which it is paid). Other examples of expenses include the cost of office expenses such as electricity and telephone, consulting, and more.

- A vendor invoice may be a bill for the purchase of expensive equipment that will be used by the company for several years. The equipment will be recorded as an asset and will be reported in the company's balance sheet section property, plant and equipment. As the equipment is utilized, its cost will be moved from the balance sheet to the income statement account Depreciation Expense.

-

Another vendor invoice may be a billing for the cost of a service that the vendor will provide in the future, but the payment must be made in advance. A common example is an insurance company's invoice for the premiums covering the next six months of insurance on the company's automobiles. The company will initially debit the invoice amount to a current asset such as Prepaid Expenses. As the insurance expires, the cost will be allocated to Insurance Expense.

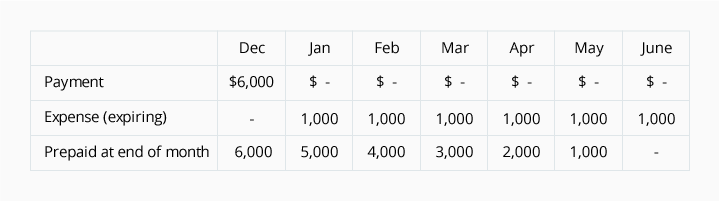

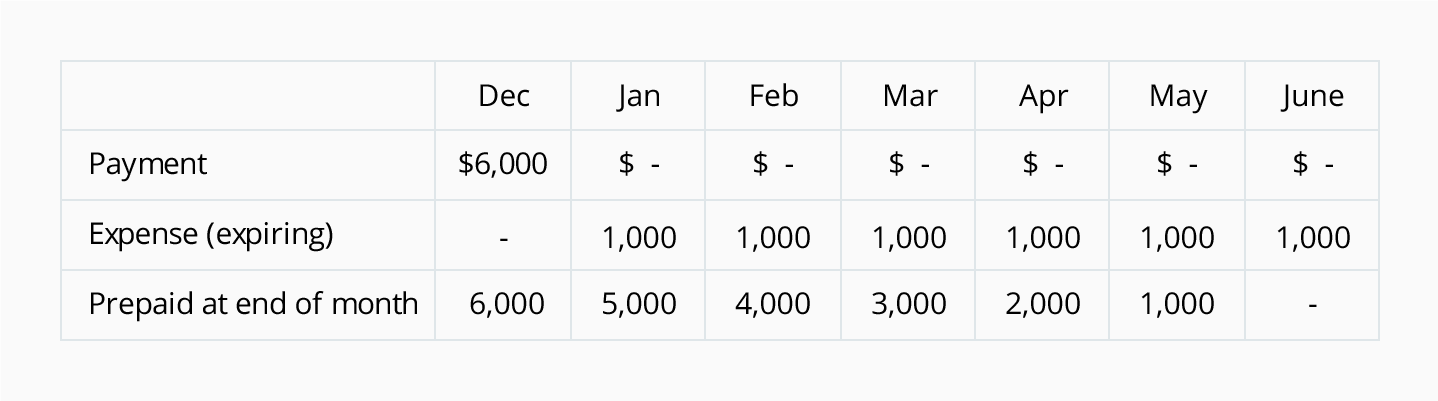

The following table illustrates an insurance premium of $6,000 that is paid in December but the coverage is for the following January 1 through June 30:

The three examples illustrate that some vendor invoices will be immediately recorded as expenses while other invoices are initially recorded as assets. The accounts payable staff needs to be instructed as to the proper accounts to be debited when vendor invoices are entered as credits to Accounts Payable. Generally, a cost that is used up and has no future economic value that can be measured is debited immediately to expense. Vendor invoices for property, plant and equipment are not expensed immediately. Instead, the cost is recorded in a balance sheet asset account and will be expensed in increments during the asset's useful life. Lastly, a prepaid expense is initially recorded in a current asset account and will be allocated to expense as the cost expires.

End of the Period Cut-Off

At the end of every accounting period (year, quarter, month, 5-week period, etc.) it is important that the accounts payable processing be up-to-date. If it is not up-to-date, the income statement for the accounting period will likely be omitting some expenses and the balance sheet at the end of the accounting period will be omitting some liabilities.

During the first few days after an accounting period ends, it is important for the accounts payable staff to closely examine the incoming vendor invoices. For example, a $900 repair bill received on January 6 may be a December repair expense and a liability as of December 31. Another vendor invoice received on January 6 maynot have been an obligation as of December 31 and is actually a January expense.

It is also necessary to review the receiving reports that have not yet been matched to vendor invoices. If items were ordered and received prior to December 31, the amounts must be recorded as of December 31 through an accrual-type adjusting entry.

Note: The proper cut-off at the end of each accounting period becomes more complicated and often more significant if a company has inventories of finished products, work-in-process and raw materials. It is possible that some goods will be included in the physical inventory counts, but the costs have not yet been recorded in Accounts Payable and in the Inventory or Purchases account.

Accruing Expenses and Liabilities

At the end of every accounting period there will be some vendor invoices and receiving reports that have not yetbeen approved or fully matched. As a result these amounts will not have been entered into the Accounts Payable account (and the related expense or asset account). These documents should be reviewed in order to determine whether a liability and an expense have actually been incurred by the company as of the end of the accounting period.

Since the accrual method of accounting requires that all of a company's liabilities and expenses must be reported on the financial statements, companies should prepare an accrual-type adjusting entry at the end of every accounting period. This adjusting entry will credit Accrued Liabilities and will debit the appropriate expense or other account for the amounts that were incurred but are not yet included in Accounts Payable. The balance in Accrued Liabilities will be reported in the current liability section of the balance sheet immediately after Accounts Payable.

It is also common for companies to prepare a reversing entry every month. The reversing entry removes the previous period's accrual adjusting entry and prevents the double-counting of an expense that could occur when the actual vendor invoice is processed.

» Tin mới nhất:

- Những Website Check Lỗi Ngữ Pháp Tiếng Anh Chất Lượng (18/05/2024)

- The writing process and assessment (18/05/2024)

- Những kinh nghiệm làm đồ án dành cho sinh viên kiến trúc (18/05/2024)

- Vai trò của các công cụ khuyến mãi đối với hành vi tiêu dùng (18/05/2024)

- Quyết định đầu tư chứng khoán và các mô hình nghiên cứu (18/05/2024)

» Các tin khác:

- General Ledger Account: Accounts Payable (21/02/2016)

- Phương pháp điều hành kinh doanh toàn cầu của IKEA và vai trò của văn hóa tổ chức (21/01/2016)

- Các lý thuyết về tiền tệ (phần 2) (18/01/2016)

- Các lý thuyết về tiền tệ (18/01/2016)

- QUY TRÌNH ĐĂNG KÝ NHÃN HIỆU TẠI CỤC SHTT (18/01/2016)

- Những chính sách về ôtô hiệu lực từ 2016 (18/01/2016)

- Sai lầm của CEO Yahoo - bài học của nhà quản lý (18/01/2016)

- Đây là bí mật sau câu hỏi tuyển dụng 'Sở thích của bạn là gì?' (18/01/2016)

- Xu Hướng Digital Marketing 2016 Tại Việt Nam (18/01/2016)

- Tại sao Yahoo màu tím, Google bảy sắc còn Facebook có màu xanh da trời? (18/01/2016)