Sample Bank Reconciliation with Amounts

In this part we will provide you with a sample bank reconciliation including the required journal entries. We will assume that a company has the following items:

| Item #1. |

The bank statement for August 2015 shows an ending balance of $3,490. |

| Item #2. |

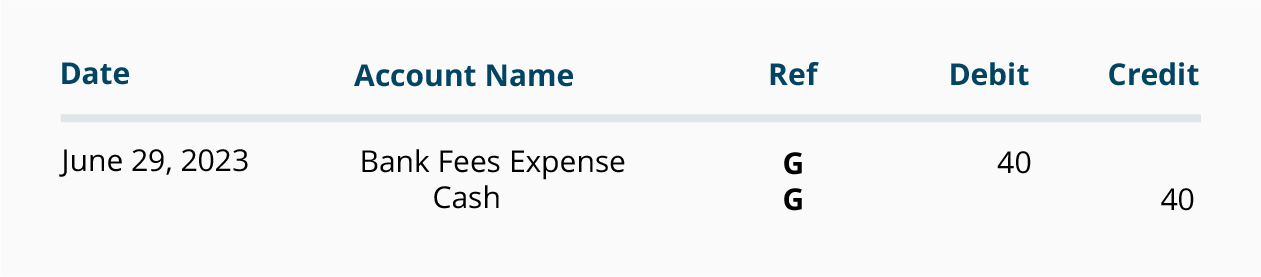

On August 31 the bank statement shows charges of $35 for the service charge for maintaining the checking account. |

| Item #3. |

On August 28 the bank statement shows a return item of $100 plus a related bank fee of $10. The return item is a customer's check that was returned because of insufficient funds. The check was also marked "do not redeposit." |

| Item #4. |

The bank statement shows a charge of $80 for check printing on August 20. |

| Item #5. |

The bank statement shows that $8 was added to the checking account on August 31 for interest earned by the company during the month of August. |

| Item #6. |

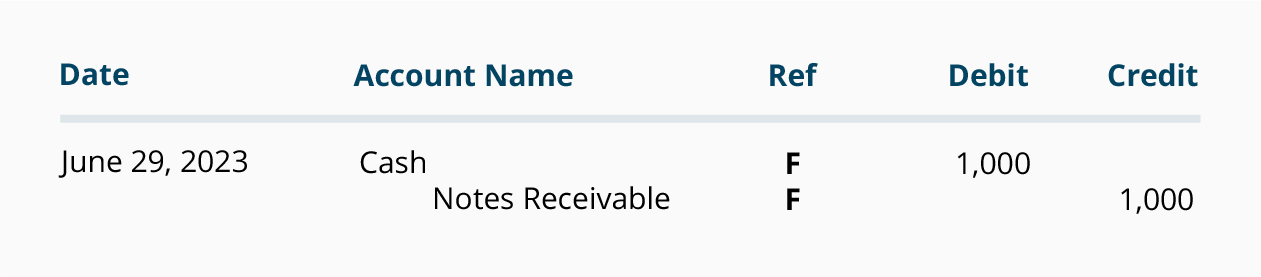

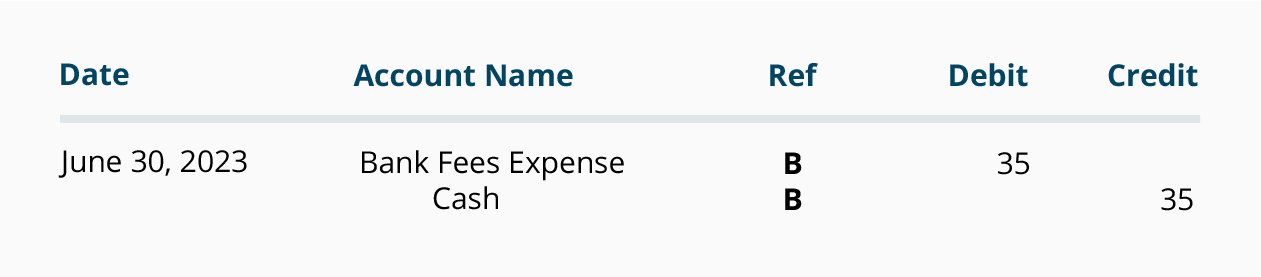

The bank statement shows that a note receivable of $1,000 was collected by the bank on August 29 and was deposited into the company's account. On the same day, the bank withdrew $40 from the company's account as a fee for collecting the note receivable. |

| Item #7. |

The company's Cash account at the end of August shows a balance of $967. |

| Item #8. |

During the month of August the company wrote checks totaling more than $50,000. As of August 31 $3,021 of the checks written in August had not yet cleared the bank and $200 of checks written in June had not yet cleared the bank. |

| Item #9. |

The $1,450 of cash received by the company on August 31 was recorded on the company's books as of August 31. However, the $1,450 of cash receipts was deposited at the bank on the morning of September 1. |

| Item #10. |

On August 29 the company's Cash account shows cash sales of $145. The bank statement shows the amount deposited was actually $154. The company reviewed the transactions and found that $154 was the correct amount. |

Before we begin our sample bank reconciliation, learn the following bank reconciliation tip.

Here's a Tip

Put it where it isn't.

If an item appears on the bank statement but not on the company's books, the item is probably going to be an adjustment to the Cash balance on (per) the company's books.

If an item is already in the company's Cash account, but has not yet appeared on the bank statement, the item is probably an adjustment to the balance per the bank statement.

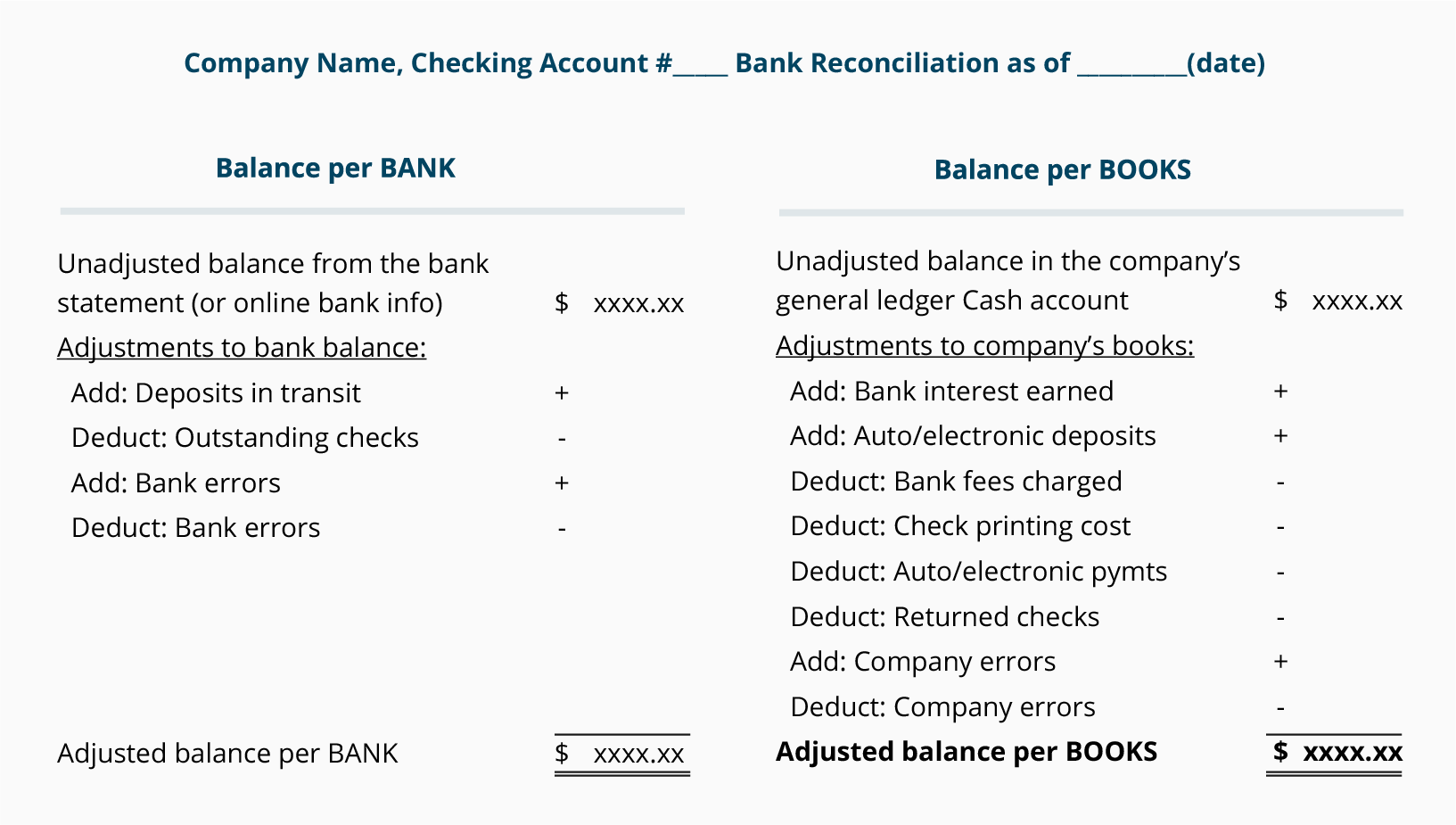

Our approach to the bank reconciliation is to prepare two schedules. The first schedule begins with the ending balance on the bank statement. We refer to this schedule as Step 1. The second schedule begins with the ending Cash account balance in the general ledger. We call this schedule Step 2.

Items 1 through 10 above have been sorted into the following schedules labeled Step 1 and Step 2. The item number is shown in the far right column of each schedule.

Step 1 Amounts

Let's review the schedule for Step 1. In all likelihood the balance shown on the bank statement is not the true balance to be reported on the company's balance sheet. The bank reconciliation process is to list the items that will adjust the bank statement balance to become the true cash balance. As the schedule for Step 1 indicates, the amount of deposits in transit must be added to the bank statement's balance. Also, the amount of checks that have been written, but not yet appearing on a bank statement, must be subtracted from the bank statement's balance. Next any bank errors should be listed and should be reported to the bank for correction. (The company does not report deposits in transit and/or outstanding checks to the bank.)

Step 2 Amounts and Required Journal Entries

Step 2 begins with the balance in the company's Cash account found in its general ledger. The bank reconciliation process includes listing the items that will adjust the Cash account balance to become the true cash balance. We will review each item appearing in Step 2 and the related journal entry that is required. Remember that any adjustment to the company's Cash account requires a journal entry. Generally, the adjustments to the books are the result of items found on the bank statement but have not yet been entered in the company's Cash account.

Item #2 Bank service charges. Since the bank deducted $35 from the company's checking account, but the company has not yet deducted this from its Cash account, the following journal entry needs to be made.

(If the annual amount of service charges is small, debit Miscellaneous Expense.)

Item #3 NSF checks and fees. Since the bank deducted these legitimate amounts from the company's bank account, the company will need to deduct these amounts from its Cash account. As mentioned, the NSF check of $100 was from a customer. Therefore, the company will likely undo the reduction to Accounts Receivable that took place when the company originally processed the $100 check. If the company wishes to recover the bank fee of $10 from the customer, it should add the $10 fee to the amount that the customer owes the company. The journal entry might look like this:

(If the amount cannot be recovered from the customer, charge an expense.)

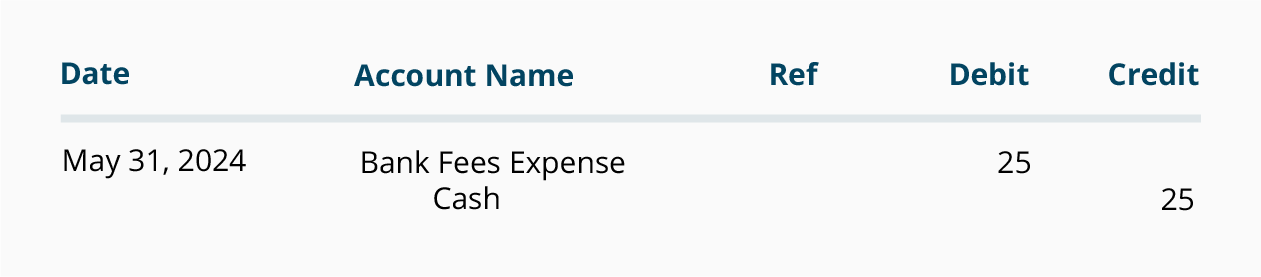

Item #4 Check printing charges. Because this expense is not yet entered on the company's books, but the amount has been deducted from its bank account, the company will make the following journal entry.

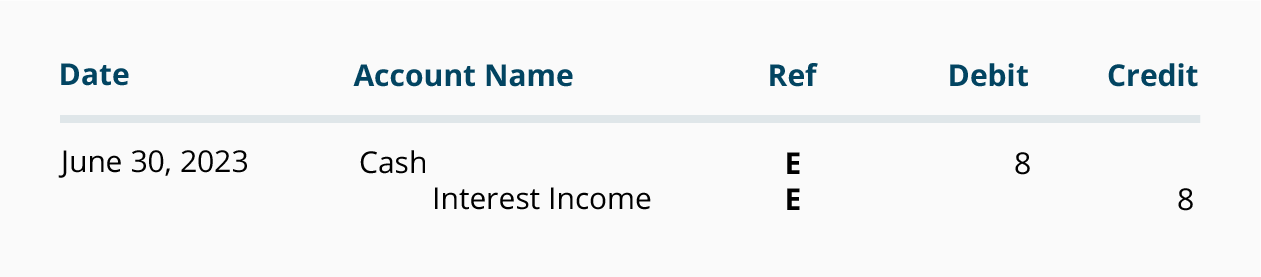

Item #5 Interest earned. The bank increased the checking account balance by $8 on August 31. Since the bank did not notify the company previously, the company must now increase the balance in its Cash account.

Item #6 Notes receivable collected. The bank increased the company's checking account when it collected a note for the company on August 29. It was determined that the company had not yet made an entry to its Cash account for this transaction. As a result the following journal entry is needed.

Item #10 Company error. The company had entered $145 in its Cash account on August 29, but the bank statement showed the correct amount: $154. The transaction involved the cash sales for the day. As a result the company's Cash account will have to be increased by $9 as follows:

Step 3 Comparing the Adjusted Balances

In the above schedules the adjusted balance for Step 1 is $1,719 and the adjusted balance for Step 2 is $1,719. The company believes that all items involving cash have been included in the schedules. As a result the company has successfully completed its bank reconciliation as of the August 31, 2015.

» Tin mới nhất:

- Cách GHI – ĐỌC dữ liệu từ tệp tin trong ngôn ngữ Java (18/12/2024)

- Những Website Check Lỗi Ngữ Pháp Tiếng Anh Chất Lượng (18/05/2024)

- The writing process and assessment (18/05/2024)

- Những kinh nghiệm làm đồ án dành cho sinh viên kiến trúc (18/05/2024)

- Vai trò của các công cụ khuyến mãi đối với hành vi tiêu dùng (18/05/2024)

» Các tin khác:

- QUAN HỆ HỢP TÁC GIỮA CÁC DOANH NGHIỆP XUẤT NHẬP KHẨU VÀ DOANH NGHIỆP LOGISTICS (18/03/2016)

- Thực trạng hoạt động đầu tư trực tiếp vào các quốc gia Asean của các ngân hàng thương mại Việt Nam (18/03/2016)

- TÍNH NĂNG MỚI TRONG VISUAL STUDIO 2015 - P2 (18/03/2016)

- TÍNH NĂNG MỚI TRONG VISUAL STUDIO 2015 - P1 (18/03/2016)

- Các quan điểm về lạm phát (18/03/2016)

- Lưu thông tiền tệ (18/03/2016)

- Khám phá 6 cách học tiếng anh hiệu quả nhanh nhất hiện nay (18/03/2016)

- Bạn đã biết 7 bí kíp viết CV tiếng Anh xin việc thuyết phục nhất? (18/03/2016)

- 5 ĐIỀU BẠN SẼ ĐẠT ĐƯỢC KHI THÀNH THẠO TIẾNG ANH (18/03/2016)

- Internet of Things mang lại sự bùng nổ kinh tế mới (18/03/2016)