Earnings Per Share

Earnings per share is not part of stockholders' equity. Nonetheless, we are including an introduction to the topic here because the calculation for earnings per share involves the stock of a corporation.

Earnings per share must appear on the face of the income statement if the corporation's stock is publicly traded. The earnings per share calculation is the after-tax net income (earnings) available for the common stockholders divided by the weighted-average number of common shares outstanding during that period.

Earnings Available for Common Stock

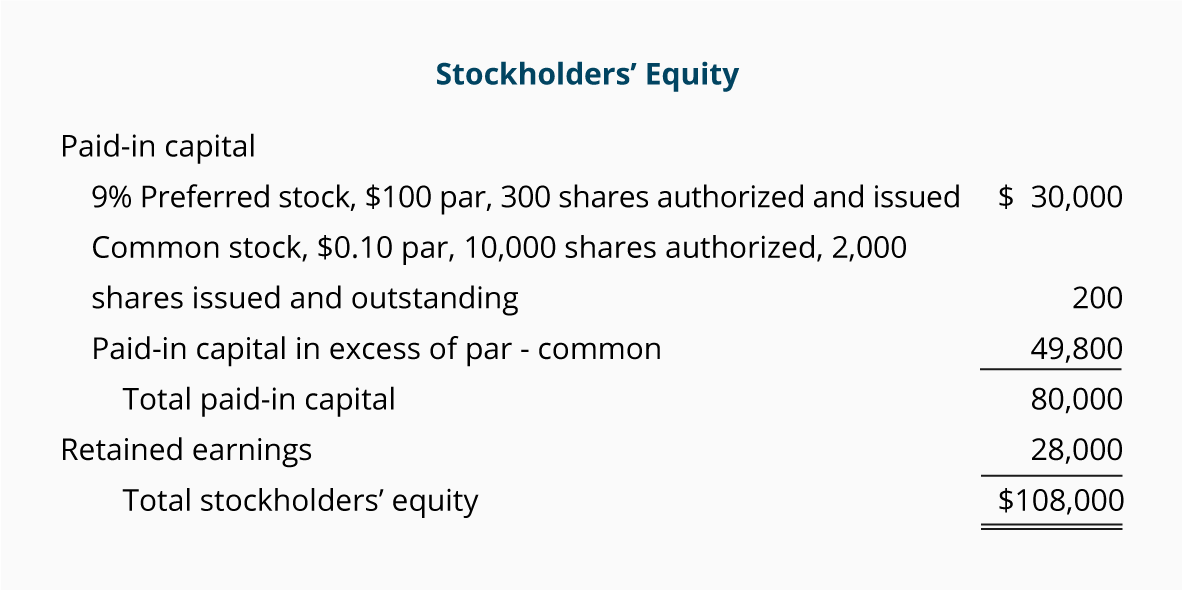

Let's assume that a corporation has the following stockholders' equity at December 31:

Additional information:

- The corporation's accounting year is the calendar year.

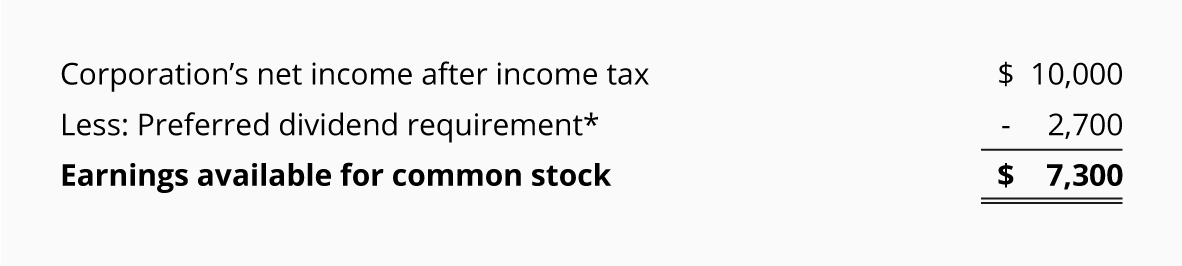

- The corporation's net income after taxes is $10,000.

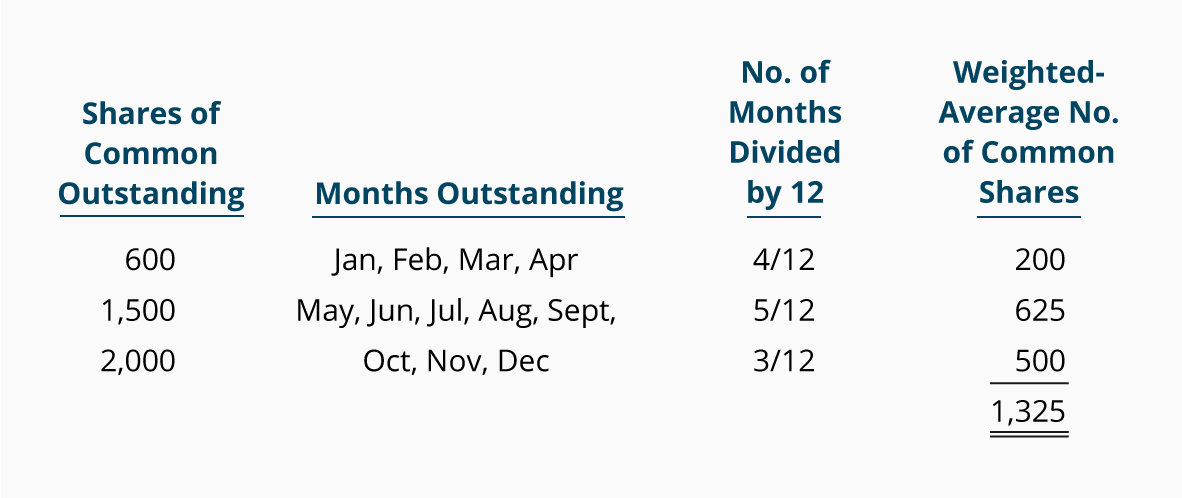

- The number of shares of common stock outstanding was 600 shares for the first four months of the year. On May 1 the corporation issued an additional 900 shares. On October 1 it issued an additional 500 shares.

- The shares of preferred stock were outstanding for the entire year.

The earnings (net income after income taxes) available for the common stockholders is:

*The preferred dividend requirement is the annual dividend of $9 per share (9% times $100 par value) times the 300 shares of preferred stock outstanding.

Weighted-Average Number of Shares of Common Stock

Since the earnings occurred throughout the entire year, we need to divide them by the number of shares that were outstanding throughout the entire year. During the first four months only 600 shares were outstanding, during the next five months 1,500 shares were outstanding, and for the final three months of the year 2,000 shares of common stock were outstanding. This situation requires that we come up with an average number of shares of common stock for the year.

As the calculation shows, the weighted-average number of shares of common stock for the year was 1,325.

It's a good idea to test this answer to be sure it's reasonable. During five of the months (May - Sep.) the number of shares of common stock outstanding was 1,500 shares. During the remainder of the year, there were more months with less than 1,500 shares outstanding. Thus, the figure of 1,325 looks reasonable.

Earnings per Share of Common Stock

After recognizing the preferred stockholders' required dividend, there was $7,300 ($10,000 minus $2,700) ofearnings available for the common stockholders. The $7,300 was earned throughout the year, so we need to divide that amount by the weighted-average number of shares of common stock outstanding throughout the year:

The earnings per share (EPS) of common stock = earnings available for common stock divided by the weighted-average number of common shares outstanding:

Other

Stock Issued for Other Than Cash

If a corporation has a limited amount of cash, but needs an asset or some services, the corporation might issue some new stock in exchange for the items needed. When stock is issued for noncash items, the items and the stock must be recorded on the books at the fair market value at the time of the exchange. Since both the stock given up and the asset or services received may have market values, accountants record the fair market value of the one that is more clearly determinable (more objective and verifiable).

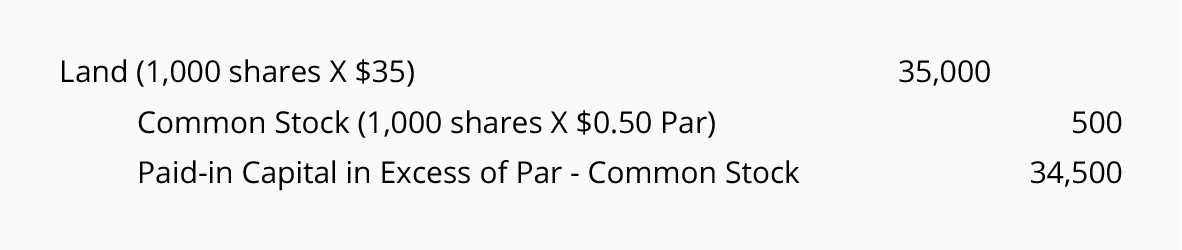

For example, if a corporation exchanges 1,000 of its publicly-traded shares of common stock for 40 acres of land, the fair market value of the stock is likely to be more clear and objective. (The stock might trade daily while similar parcels of land in the area may sell once every few years.) In other situations, the common stock might rarely trade while the value of the received service is well-established.

To illustrate, let's assume that 1,000 shares of common stock are exchanged for a parcel of land. The stock is publicly traded and recent trades have been at $35 per share. The par value is $0.50 per share. The land's fair market value is not as clear since there has not been a comparable sale during the past four years.

The entry made to record the exchange will show the land at the fair market value of the common stock, since the stock's fair market value is more clear and objective than someone's estimate of the current value of the land:

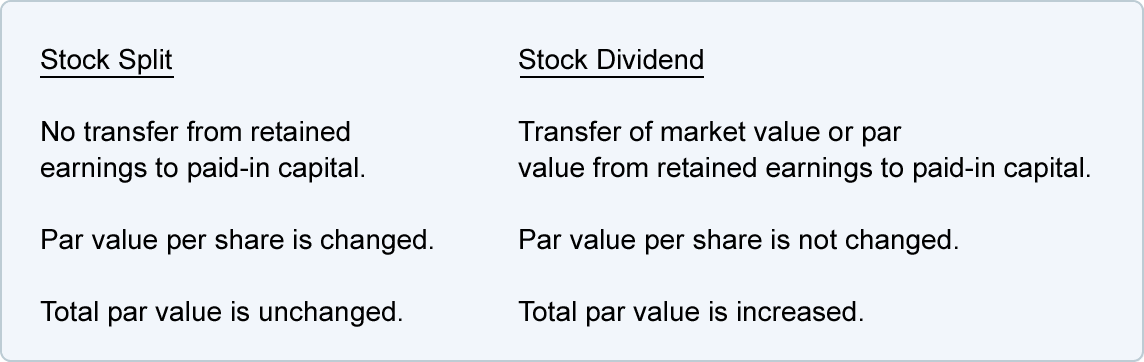

Differences in Accounting for Stock Splits Vs. Stock Dividends

» Tin mới nhất:

- Cách GHI – ĐỌC dữ liệu từ tệp tin trong ngôn ngữ Java (18/12/2024)

- Những Website Check Lỗi Ngữ Pháp Tiếng Anh Chất Lượng (18/05/2024)

- The writing process and assessment (18/05/2024)

- Những kinh nghiệm làm đồ án dành cho sinh viên kiến trúc (18/05/2024)

- Quyết định đầu tư chứng khoán và các mô hình nghiên cứu (18/05/2024)

» Các tin khác:

- Sample Bank Reconciliation with Amounts (23/03/2016)

- QUAN HỆ HỢP TÁC GIỮA CÁC DOANH NGHIỆP XUẤT NHẬP KHẨU VÀ DOANH NGHIỆP LOGISTICS (18/03/2016)

- Thực trạng hoạt động đầu tư trực tiếp vào các quốc gia Asean của các ngân hàng thương mại Việt Nam (18/03/2016)

- TÍNH NĂNG MỚI TRONG VISUAL STUDIO 2015 - P2 (18/03/2016)

- TÍNH NĂNG MỚI TRONG VISUAL STUDIO 2015 - P1 (18/03/2016)

- Các quan điểm về lạm phát (18/03/2016)

- Lưu thông tiền tệ (18/03/2016)

- Khám phá 6 cách học tiếng anh hiệu quả nhanh nhất hiện nay (18/03/2016)

- Bạn đã biết 7 bí kíp viết CV tiếng Anh xin việc thuyết phục nhất? (18/03/2016)

- 5 ĐIỀU BẠN SẼ ĐẠT ĐƯỢC KHI THÀNH THẠO TIẾNG ANH (18/03/2016)