Bond Discount with Straight-Line Amortization

When a corporation is preparing a bond to be issued/sold to investors, it may have to anticipate the interest rate to appear on the face of the bond and in its legal contract. Let's assume that the corporation prepares a $100,000 bond with an interest rate of 9%. Just prior to issuing the bond, a financial crisis occurs and the market interest rate for this type of bond increases to 10%. If the corporation goes forward and sells its 9% bond in the 10% market, it will receive less than $100,000. When a bond is sold for less than its face amount, it is said to have been sold at a discount. The discount is the difference between the amount received (excluding accrued interest) and the bond's face amount. The difference is known by the terms discount on bonds payable, bond discount, or discount.

To illustrate the discount on bonds payable, let's assume that in early December 2014 a corporation prepares a 9% $100,000 bond dated January 1, 2015. The interest payments of $4,500 ($100,000 x 9% x 6/12) will be required on each June 30 and December 31 until the bond matures on December 31, 2019.

Next, let's assume that just prior to offering the bond to investors on January 1, the market interest rate for this bond increases to 10%. The corporation decides to sell the 9% bond rather than changing the bond documents to the market interest rate. Since the corporation is selling its 9% bond in a bond market which is demanding 10%, the corporation will receive less than the bond's face amount.

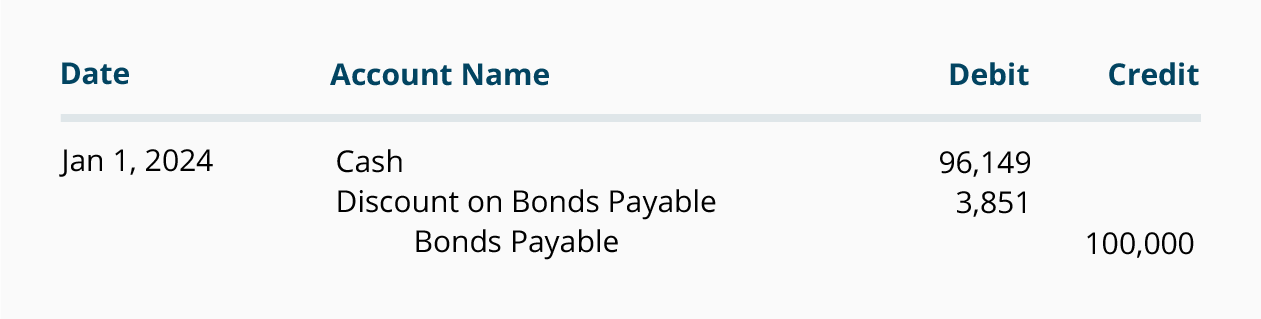

To illustrate the accounting for bonds payable issued at a discount, let's assume that the 9% bond is sold in the 10% market for $96,149 plus $0 accrued interest on January 1, 2015. The corporation's journal entry to record the sale of the bond will be:

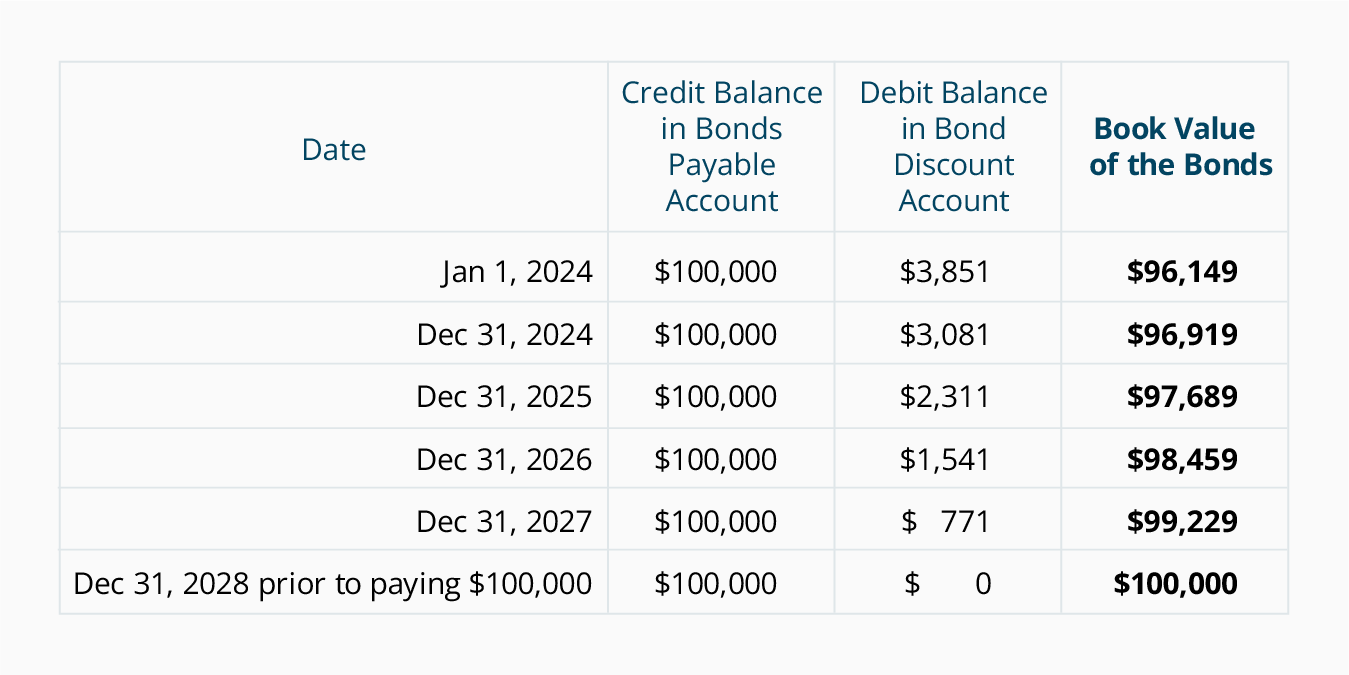

The account Discount on Bonds Payable (or Bond Discount or Unamortized Bond Discount) is a contra liability account since it will have a debit balance. Discount on Bonds Payable will always appear on the balance sheet with the account Bonds Payable. In other words, if the bond is a long-term liability, both Bonds Payable and Discount on Bonds Payable will be reported on the balance sheet as long-term liabilities. The combination or net of these two accounts is known as the book value or the carrying value of the bonds. On January 1, 2015 the book value of this bond is $96,149 (the $100,000 credit balance in Bonds Payable minus the debit balance of $3,851 in Discount on Bonds Payable.)

Discount on Bonds Payable with Straight-Line Amortization

Over the life of the bond, the balance in the account Discount on Bonds Payable must be reduced to $0. Reducing this account balance in a logical manner is known as amortizing or amortization. Since a bond's discount is caused by the difference between a bond's stated interest rate and the market interest rate, the journal entry for amortizing the discount will involve the account Interest Expense.

In our example, the bond discount of $3,851 results from the corporation receiving only $96,149 from investors, but having to pay the investors $100,000 on the date that the bond matures. The discount of $3,851 is treated as an additional interest expense over the life of the bonds. When the same amount of bond discount is recorded each year, it is referred to as straight-line amortization. In this example, the straight-line amortization would be $770.20 ($3,851 divided by the 5-year life of the bond).

Straight-Line Amortization of Bond Discount on Annual Financial Statements

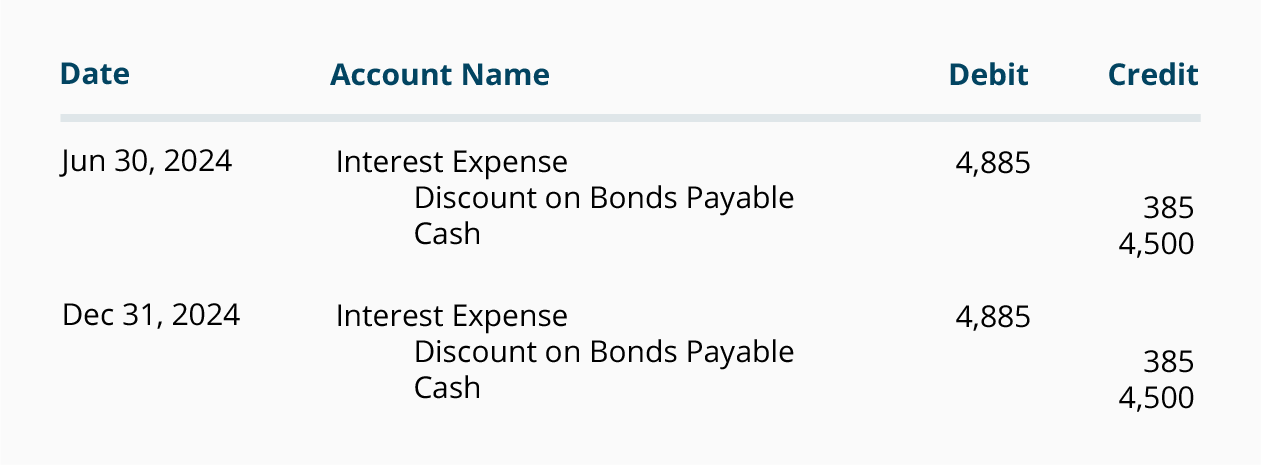

If a corporation issues only annual financial statements on December 31, the amortization of bond discount is often recorded at the time of its semiannual interest payments. In our example the journal entries for 2015 under the straight-line method will be:

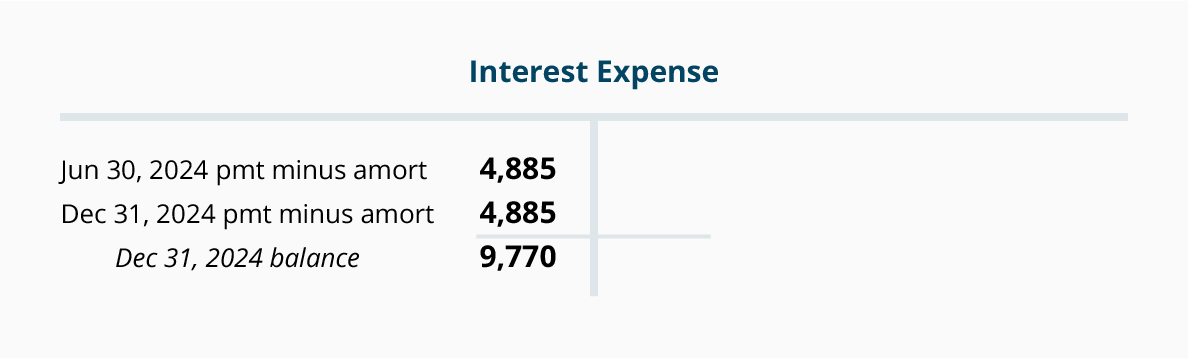

The interest expense for the year 2015 will be $9,770 (the two semiannual interest payments of $4,500 each plus the two semiannual amortizations of bond discount of $385 each). The following T-account for Interest Expense shows the entries for the year 2015:

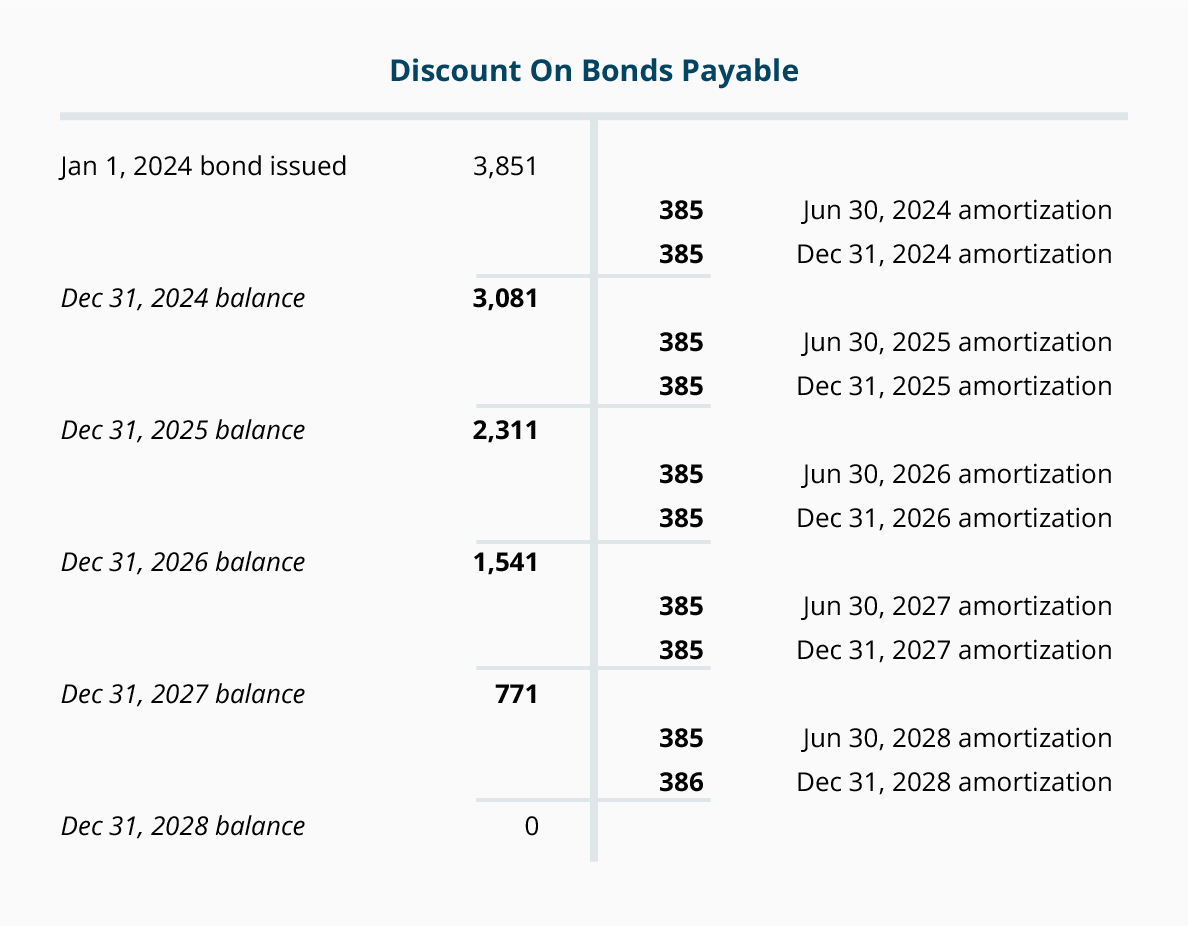

The following T-account shows how the balance in Discount on Bonds Payable will be decreasing over the 5-year life of the bond.

As the bond discount is amortized, the bond's book value will be increasing from $96,149 on the date the bond was issued to the bond's maturity amount of $100,000:

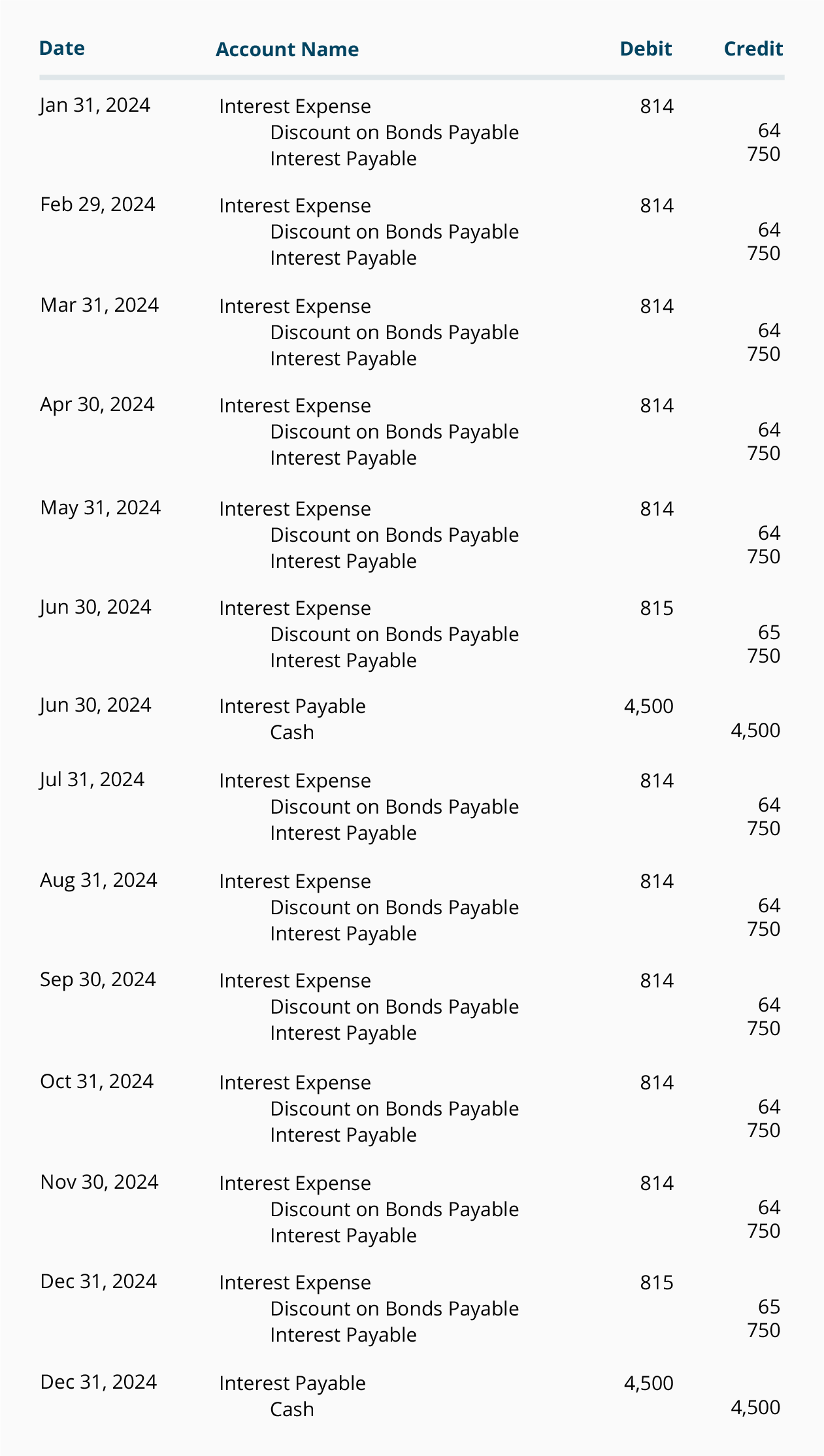

Straight-Line Amortization of Bond Discount on Monthly Financial Statements

If the corporation issues monthly financial statements, the monthly amount of bond discount amortization under the straight-line method will be $64.18 ($3,851 of bond discount divided by the bond's life of 60 months). The 12 monthly journal entries for the bond interest and amortization of bond discount plus the entries for the June 30 and December 31 semiannual interest payments will result in the following 14 entries during the year 2015:

The journal entries for the remaining years will be similar if all of the bonds remain outstanding.

» Tin mới nhất:

- Cách GHI – ĐỌC dữ liệu từ tệp tin trong ngôn ngữ Java (18/12/2024)

- Những Website Check Lỗi Ngữ Pháp Tiếng Anh Chất Lượng (18/05/2024)

- The writing process and assessment (18/05/2024)

- Những kinh nghiệm làm đồ án dành cho sinh viên kiến trúc (18/05/2024)

- Quyết định đầu tư chứng khoán và các mô hình nghiên cứu (18/05/2024)

» Các tin khác:

- Bond Premium with Straight-Line Amortization (16/06/2016)

- Kỹ năng học trong 10 phút có thể thay đổi cuộc đời mãi mãi (19/05/2016)

- Các xu thế tự do hóa thương mại của khối ASEAN trong những thập niên gần đây (18/05/2016)

- TRỞ NGẠI KINH TẾ CỦA DOANH NGHIỆP NHỎ VÀ VỪA TẠI VIỆT NAM (18/05/2016)

- Service capacity (18/05/2016)

- Operation and Supply Chain Strategy (18/05/2016)

- NHỮNG PHI VỤ KINH DOANH MƯỢN GIÓ BẺ MĂNG( 2 ) (18/05/2016)

- NHỮNG PHI VỤ KINH DOANH MƯỢN GIÓ BẺ MĂNG( 1 ) (18/05/2016)

- VAI TRÒ CỦA NGÂN HÀNG TRUNG ƯƠNG ĐỐI VỚI ỔN ĐỊNH TÀI CHÍNH (18/05/2016)

- Ngân hàng đâu chỉ cạnh tranh bằng lãi suất (18/05/2016)