General Discussion of Income Statement

The income statement has some limitations since it reflects accounting principles. For example, a company's depreciation expense is based on the cost of the assets it has acquired and is using in its business. The resulting depreciation expense may not be a good indicator of the economic value of the asset being used up. To illustrate this point let's assume that a company's buildings and equipment have been fully depreciated and therefore there will be no depreciation expense for those buildings and equipment on its income statement. Is zero expense a good indicator of the cost of using those buildings and equipment? Compare that situation to a company with new buildings and equipment where there will be large amounts of depreciation expense.

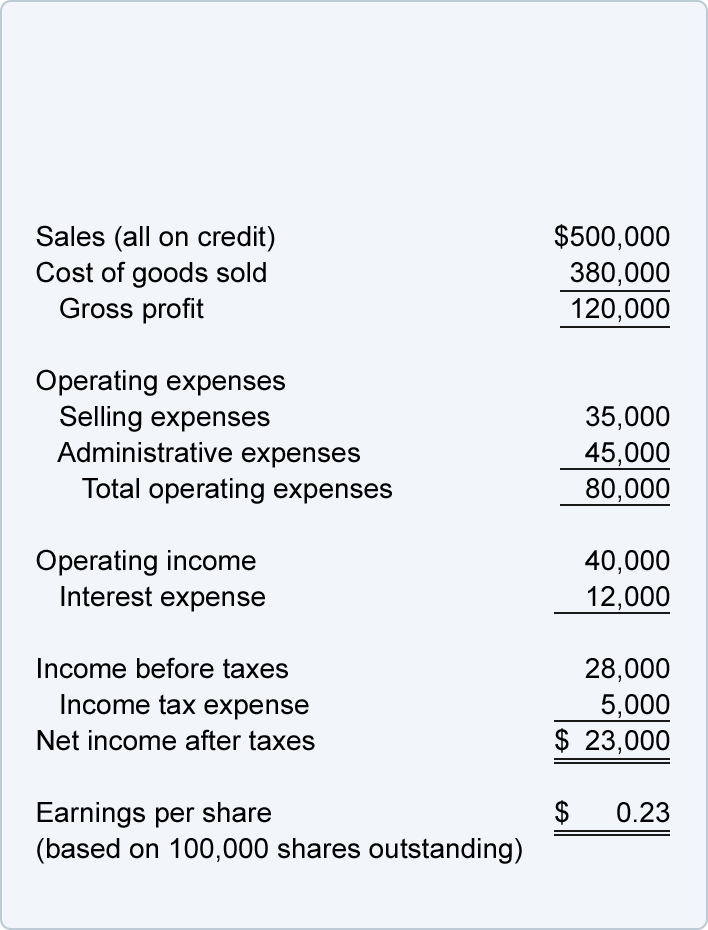

The remainder of our explanation of financial ratios and financial statement analysis will use information from the following income statement:

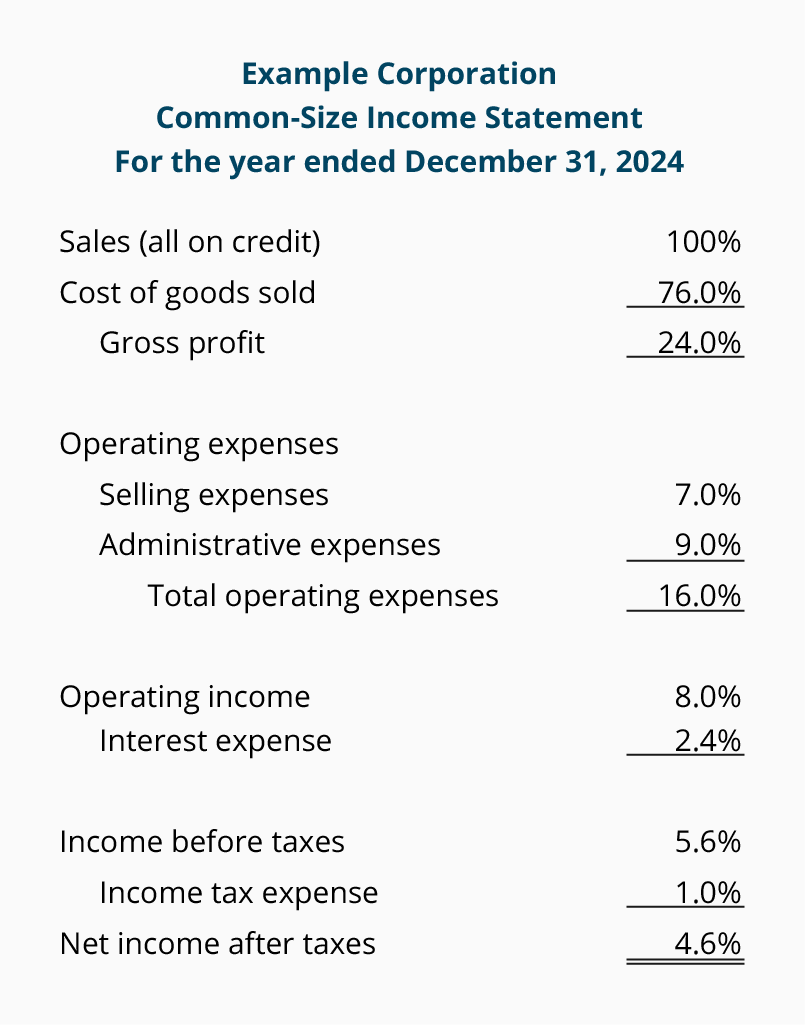

Common-Size Income Statement

Financial statement analysis includes a technique known as vertical analysis. Vertical analysis results in common-size financial statements. A common-size income statement presents all of the income statement amounts as a percentage of net sales. Below is Example Corporation's common-size income statement after each item from the income statement above was divided by the net sales of $500,000:

The percentages shown for Example Corporation can be compared to other companies and to the industry averages. Industry averages can be obtained from trade associations, bankers, and library reference desks. If a company competes with a company whose stock is publicly traded, another source of information is that company's "Management's Discussion and Analysis of Financial Condition and Results of Operations" contained in its annual report to the Securities and Exchange Commission (SEC). This annual report is the SEC Form 10-K and is usually accessible under the "Investor Relations" tab on the corporation's website.

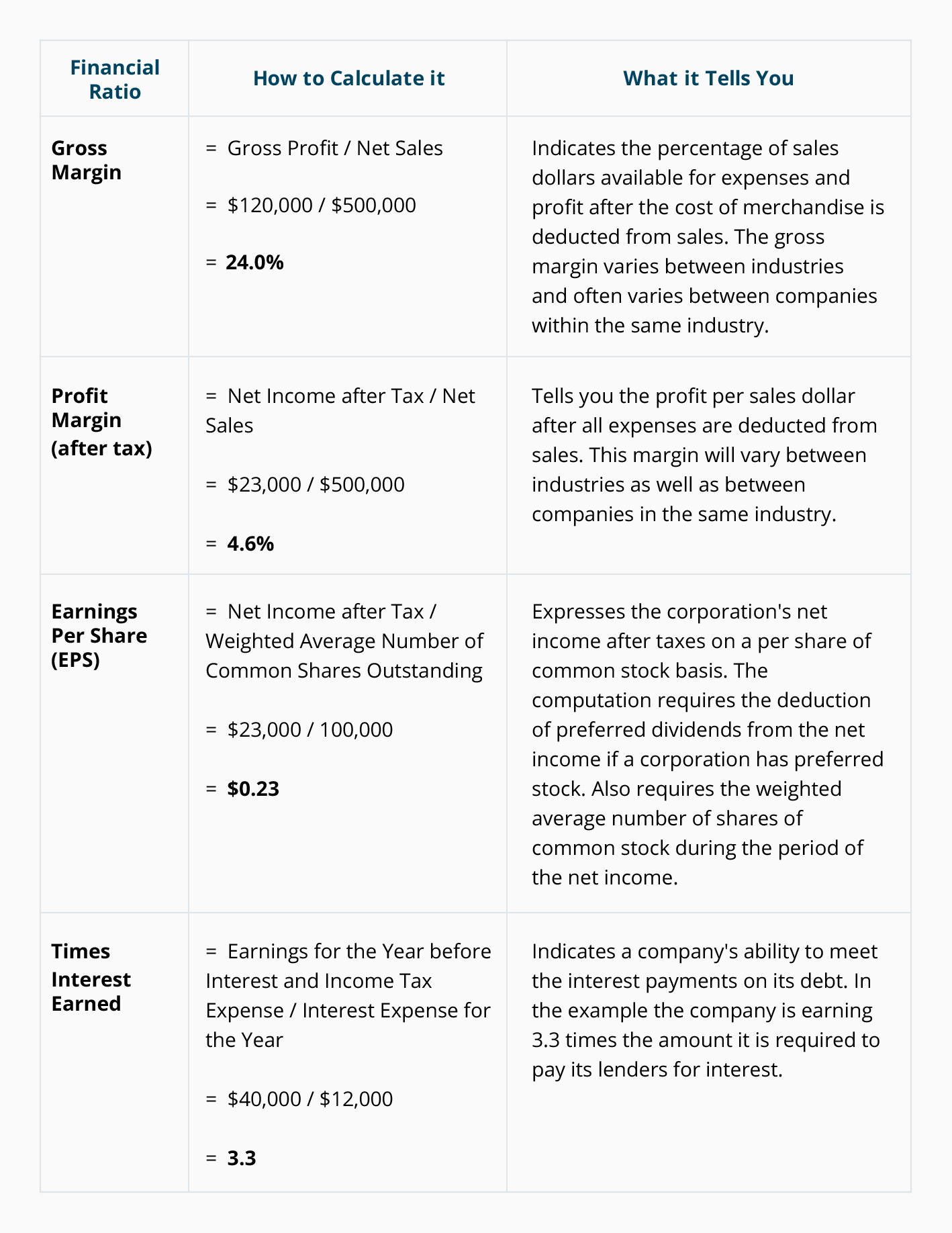

Financial Ratios Based on the Income Statement

» Tin mới nhất:

- Cách GHI – ĐỌC dữ liệu từ tệp tin trong ngôn ngữ Java (18/12/2024)

- Những Website Check Lỗi Ngữ Pháp Tiếng Anh Chất Lượng (18/05/2024)

- The writing process and assessment (18/05/2024)

- Những kinh nghiệm làm đồ án dành cho sinh viên kiến trúc (18/05/2024)

- Quyết định đầu tư chứng khoán và các mô hình nghiên cứu (18/05/2024)

» Các tin khác:

- Cải cách dịch vụ hành chính công ở Việt Nam hiện nay và những vấn đề đặt ra (18/10/2016)

- THỦ TỤC HẢI QUAN ĐIỆN TỬ TỪNG BƯỚC ĐÁP ỨNG CÁC TIÊU CHUẨN QUỐC TẾ VỀ HẢI QUAN HIỆN ĐẠI (18/10/2016)

- Một "con hổ" khác của Châu Á (18/10/2016)

- Công việc tương lai - những kỹ năng cần thiết (18/10/2016)

- Bitcoin- xu thế thời công nghệ ( phần 1) (18/10/2016)

- Bao thanh toán ở Việt Nam (18/10/2016)

- FPT Retail bắt tay Vinamilk mở chuỗi cửa hàng bán lẻ (18/10/2016)

- FPT Retail bắt tay Vinamilk mở chuỗi cửa hàng bán lẻ (18/10/2016)

- Marketing địa phương (18/10/2016)

- Ngoại hối và thị trường ngoại hối (18/10/2016)