Format of the Statement of Cash Flows

The statement of cash flows has four distinct sections:

- Cash involving operating activities

- Cash involving investing activities

- Cash involving financing activities

- Supplemental information.

Assuming that the cash flow statement is being prepared using the indirect method (the method used by most companies) the differences in a company's balance sheet accounts will provide much of the needed information. For example, if the statement of cash flows is for the year 2015, the balance sheet accounts at December 31, 2015 will be compared to the balance sheet accounts at December 31, 2014. The changes—or differences—in these account balances will likely be entered in one of the sections of the statement of cash flows.

Shown below is each of the four sections of the statement of cash flows, followed by a list of those balance sheet accounts which affect it.

1. Cash Provided From or Used By Operating Activities

This section of the cash flow statement reports the company's net income and then converts it from the accrual basis to the cash basis by using the changes in the balances of current asset and current liability accounts, such as:

Accounts Receivable

Inventory

Supplies

Prepaid Insurance

Other Current Assets

Notes Payble

Accounts Payable

Wages Payable

Payroll Taxes Payable

Interest Payable

Income Taxes Payable

Unearned Revenues

Other Current Liabilities

In addition to using the changes in current assets and current liabilities, the operating activities section has adjustments for depreciation expense and for the gains and losses on the sale of long-term assets.

2. Cash Provided From or Used By Investing Activities

This section of the cash flow statement reports changes in the balances of long-term asset accounts, such as:

Long-term Investments

Land

Buildings

Equipment

Furniture & Fixtures

Vehicles

In short, investing activities involve the purchase and/or sale of long-term investments and property, plant, and equipment.

3. Cash Provided From or Used By Financing Activities

This section of the cash flow statement reports changes in balances of the long-term liability and stockholders' equity accounts, such as:

Notes Payable (generally due after one year)

Bonds Payable

Deferred Income Taxes

Preferred Stock

Paid-in Capital in Excess of Par-Preferred Stock

Common Stock

Paid-in Capital in Excess of Par-Common Stock

Paid-in Capital from Treasury Stock

Retained Earnings

Treasury Stock

In short, financing activities involve the issuance and/or the repurchase of a company's own bonds or stock as well as short-term and long-term borrowings and repayments.

4. Supplemental Information

This section of the cash flow statement discloses the amount of interest and income taxes paid. Also reported are significant exchanges not involving cash. For example, the exchange of company stock for company bonds would be reported in this section.

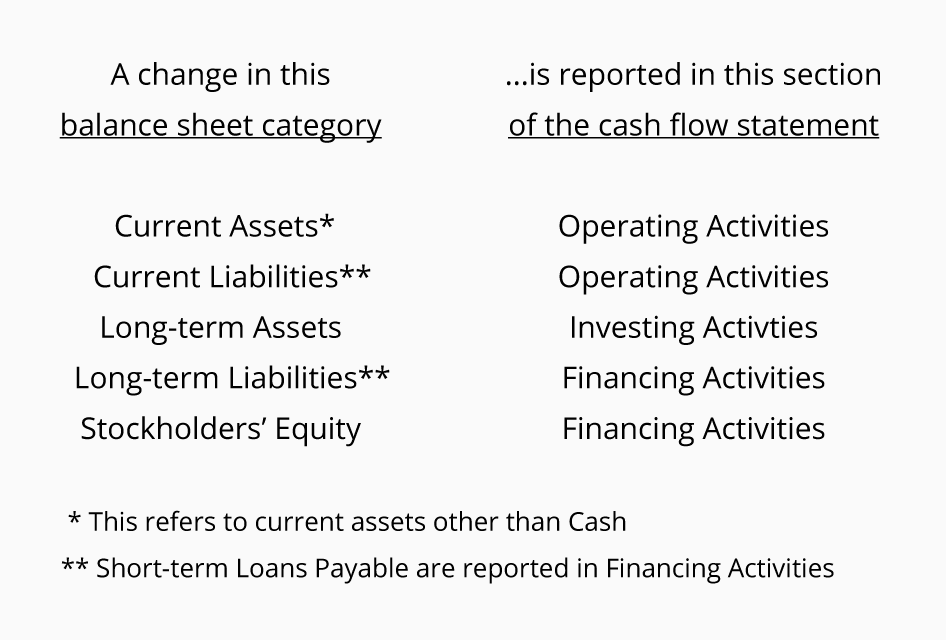

Where To Enter The Balance Sheet Changes

Take a look at the summary below—it shows where the changes in balance sheet accounts should be entered on your statement of cash flows:

» Tin mới nhất:

- Nhận biết "Điểm mù" trong đầu tư chứng khoán (24/04/2024)

- Kho vũ khí tuyệt vời để xây dựng kỹ năng viết tiếng Anh cho sinh viên (18/04/2024)

- CÁC YẾU TỐ BỊ LOẠI TRỪ KHI TÍNH GDP (18/04/2024)

- Chiến lược tăng trưởng quốc tế của Tesco (18/04/2024)

- Barra tại GM đối mặt với những thách thức (18/04/2024)

» Các tin khác:

- Basic Accounting Principles and Guideline (11/05/2016)

- 5 qui tắc Nói bạn cần biết! khi muốn có khả năng nói Tiếng Anh thông thạo (11/05/2016)

- BÍ QUYẾT LUYỆN NÓI TIẾNG ANH HIỆU QUẢ (11/05/2016)

- Những lỗi phổ biến trong trình bày bằng Powerpoint (10/05/2016)

- Điều chỉnh quy định tuyển sinh đại học năm 2016 (20/04/2016)

- Quà Tặng: Một Kênh Marketing Hiệu Quả (20/04/2016)

- 8 Chiến Lược Tăng Doanh Số Bán Hàng Với Instagram (20/04/2016)

- Sales Và Marketing: Vũ Điệu Không Đồng Bộ (20/04/2016)

- Rủi Ro Của Chiến Thuật Hạ Giá (20/04/2016)

- Bất ngờ với kế hoạch trồng khoai tây của NASA trên sao Hoả (19/04/2016)